StableCoin Deep Dive - MetricsDAO

In this Dashboard I will take a look at the different types of stablecoin, stablecoin pegging, the recent depegging of UST & what measures are taken by US Dollar stablecoins to ensure they stay pegged.

A stablecoin in simple terms is a cryptocurrency pegged to the value of another asset with the most common assets being fiat currency and commodities such as Gold & Silver. The first-ever stable coin BITUSD was released on the 21st of July 2014, it was a crypto collaterasied asset.

With people more commonly buying cryptocurrency with FIAT currency, stablecoins pegged to FIAT allow investors a way of storing the value of their FIAT currency on the blockchain for quick use. They also can be used during market dips as a way of swapping to a stablecoin to avoid further loses removing the need to swap to fiat.

9 out of 10 of the top trading pairs on the largest exchange Binance have a stablecoin as the accompanying asset, accounting for billions of pounds in volume. With the majority of the top DEFI protocol MakerDAOs total value locked coming from collecting crypto as collateral to mint the stablecoin DAI. This highlights both the popularity of stablecoins and how closely tied they are to the crypto market as a whole.

There are two main types of stablecoin, collateralised and algorithmic.

An algorithmic stablecoin uses an algorithm to maintain its pegging to a currency and a collateralised stable coin is backed by either crypto, fiat and real-world reserves. Let's take a look at a few well-known stablecoins that demonstrate this.

USDT, BUSD, TUSD and USDC are collateralised stable coins, majority backed by a mix of fiat and real-world reserves which can consist of majority holdings of US dollar, alongside, commodities and bonds. They aim to be backed 1 to 1 with assets in their reserves.

GUSD is also a collaterasied stablecoin being the first dollar back stable coin to get regulatory approval from the U.S. government. It is backed one to one with USD and holders can redeem it for an equivalent amount of USD on the Gemini platform.

DAI issued by MakerDAO is an algorithmic stablecoin which is backed by a number of crypto assets(Multi-Collatrised), you can lend assets including ETH, BTC, UNI, YFI, MANA, MATIC and more in order to mint DAI. The assets lent to MakerDAO back the value of the stablecoin DAI. DAI is over collateralised meaning you lend more to Maker DAO than you mint in DAI.

FRAX stable coin takes a two-pronged approach being backed by collateral and being algorithmic. FRAX collaterisation changes over time with it currently being backed by 89.50% of collateral, this collateral is in the form other stablecoins and crypto assets used to mint FRAX. FRAX believes that over time with the growth of the protocol investors will accept a lower level of collaterisation. The algorithmic element of FRAX burns and mints Frax Shares(FXS) in order to maintain the stablecoin pegging of FRAX. Read more about how FRAX stablecoin works here : FRAX a Fractional Algorithmic Stablecoin.

Let's take some time to look at UST separate from the other stablecoins I mentioned, as you will have noticed most of the USD stablecoins mentioned above either have a number of assets in the collateral they use to back their stablecoin, whether that be used to maintain the price algorithmically or not.

UST however used an algorithmic arbitrage system to maintain the backing of their stablecoin with reliance on 1 coin to maintain its pegging once it went below its pegging price Luna:

How Arbitrage Worked with UST & LUNA:

UST value is maintained when it is below 1$ by allowing anyone to swap UST for 1$ worth of Luna, if the price of UST dropped to 0.90, anyone can swap 1 UST for $1 worth of Luna, and sell $1 Luna for 1 USDT, banking $0.10 profit. Swapping UST for Luna burns UST, reducing the supply and increasing its value.

When the value of UST is above $1 (for example, 1 UST = 1.10 USDT), one can swap 1 UST for 1.10 USDT. Buy $1.10 worth of Luna. Then swap $1 worth of Luna for 1$ UST, allowing you to make 0.10 USD profit. Swapping from Luna to UST natively mints UST, increasing the supply of UST and bringing the value down over time.

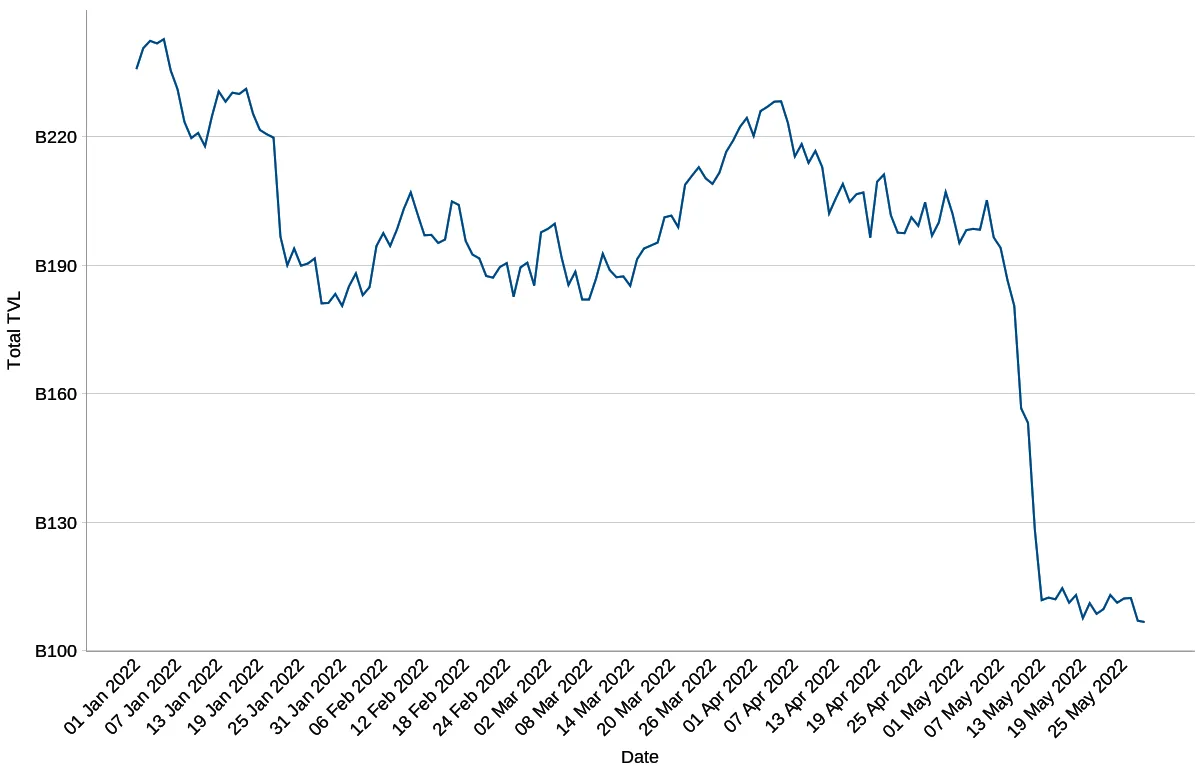

Total Value Locked DEFI - DEFI Lama

Shortly following the UST deppegging we see the largest outflow of value year to date, with 24 billion being sent to CEX at its peak, as soon as the difference between UST and it's peg began to approach a cent we can see an increase in outflow. When the peg came close to being restored the outflow slowed on the 8th of May, but when the peg began to fall the following day outflow increases by billions, with a 846% increase seen from when the peg was relatively stable on the 1st of May and the peak of outflow on May 24th.

The effect of the deppeging of UST also impacted DEFI, with the TVL of DEFI dropping by half shortly after UST was deppeged.

The assets most sent to CEXs during UST depegging were mostly stablecoins, with Luna being sent to exchanges due to the close relationship it has with UST. While a few other cryptos were sent to exchanges, it shows how the depegging of UST impacted other stable coins.

At the start of the month when the price of UST is relatively stable we can see that while outflow to CEXs are made up mostly of stablecoins, it sits at around 60%, the percentage outflow increases as UST depegs and so does the amount of stablecoin outflow daily.

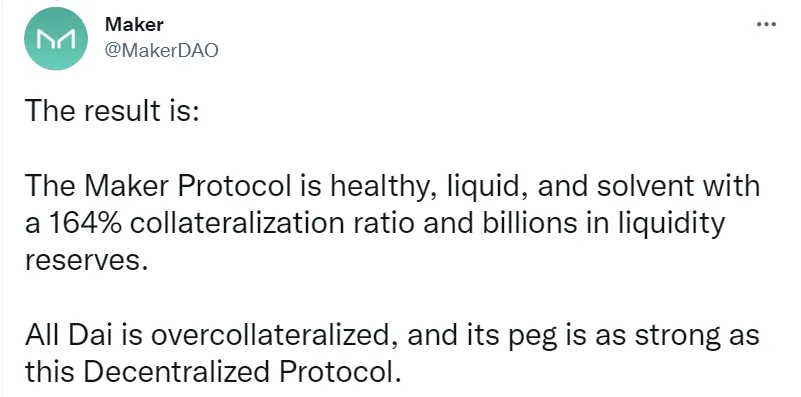

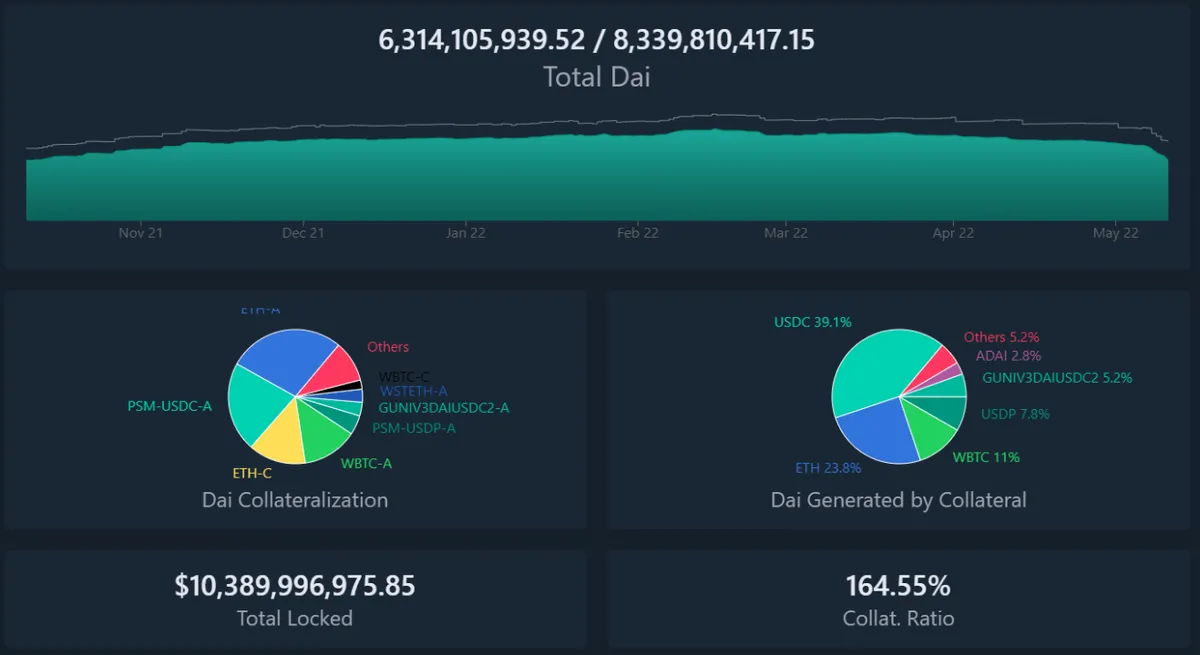

The depegging of UST also impacted the circulating supply of DAI, with investors repaying billions of DAI at the beginning of the depegging of UST. The falling of UST could have encouraged investors to repay their DAI to receive their underlying assets, as they may have become worried about whether DAI would maintain its dollar peg. From May 5th to May 14th, a total of 5.37 billion DAI was repaid with over a billion dollars of DAI being reclaimed on 2 days during that period. Importantly due to over collateriastion on the Maker Dao platform, the reclaiming of DAI had a negligible impact on the price of DAI. MakerDAO created a Twitter thread, during the beginning the UST depegging to address how the protocol works:

The price of a USD stablecoin is expected to be as close to a Dollar as possible, while some variation is accepted, generally stablecoins stay within less than a fraction of a cent of their pegging most of the time. For use within exchanges this can be especially important as investors will assume a stablecoin paired with another asset will reflect the real-world valuation of the cost of the other asset, i.e if ETH is worth 1750 USDT, ETH is worth 1750 dollars. Within the context of DEFI, dips below can mean that actualised returns on an interest-bearing account are less and with a number of exchanges becoming intermediaries between DEFI platforms, the reputation of a CEX can be at risk if pegging isn't consistent and they offer yield on an asset to their users.

Generally the majority of them stayed relatively close to their pegging, USDT dropped to 97 cents at it's low which was a worry for investors. During moments when USDT drops below a dollar users can redeem USDT tokens for the equivalent amount of USD. Reducing the circulating supply of USDT and helping to restore its pegging. So far Tether has paid out 10 billion dollars in withdrawals. FRAX a partially algorithmic stable coin saw a dip to 0.984$ on May 11th showing a possible limitation of algorithmic stablecoins. All other stablecoins stayed close to pegging.

• For the chart Stablecoins Value Year To Day the data is taken from fact_hourly_token_prices, with the stablecoins DAI, BUSD, USDC, FRAX, TUSD, GUSD and USDT being represented in the data. The average price of all the coins daily is represented in the chart.

• For the chart UST Price Year To Date the data is taken from fact_hourly_token_prices with the stablecoin UST being selected. The token price is represented hourly.

• For the chart Outflow of all Coins on ETH to CEX and UST Price, data is taken from Ethereum_core, with Ez_token_transfers joined with dim_labels to find addresses with the label CEX. Data is taken from the year to date. with the Sum of USD sent to CEX being represented by the outflow amount. The price of UST is also represented in this chart, with the average price being represented daily, the data for this is taken from fact_token_price_hourly.

• For the chart Average Price Of Gold Stablecoins the data is taken from fact_hourly_token_prices with the stablecoins XUAt and PAXG being selected. The token price is represented daily, with the average price being selected using the AVG function.

• For the chart Number of Transactions Gold Stablecoins the data is taken from ethereum.core.ez_token_transfers with the stablecoins XUAt and PAXG being selected. The sum of the daily transactions is calculated using a distinct count on TX Hash and grouping them daily and based on the stable coin symbol.

• For the chart Outflow To Cex, Percentage of outflow stablecoin., data is taken from Ethereum_core, with Ez_token_transfers joined with dim_labels to find addresses with the label CEX. Stablecoins included are DAI, GUSD, BUSD, USDC, MIM, USDT, PAX, UST, TUSD, USDN, USDD and the euro stablecoin EURS. Data is taken from the month of May and with the Sum of USD sent to CEX being represented by the outflow amount. Percentage of stablecoins is calculated by dividing, the outflow amount of stablecoins by the outflow amount and times the answer by 100.

• 20 Most Sent To Cex Assets During Depegging of UST charts data is taken from Ethereum_core, with Ez_token_transfers table joined with dim_labels to find addresses with the label CEX. Data is taken from 9th of May to the 21st of May, which represents the majority of the volume post deppeging of UST.

• The data for the charts Stablecoin Max Price May and Stablecoin Minimum Price May are taken from the table fact_hourly_token_prices with the minimum price being selected for MIM, DAI, USDT, BUSD and USDC. The same coins are selected from MAX price, data is taken from the month of May.

• Data for the chart Total Value Locked DEFI is taken from the CSV file on the DEFI Lama website with the TVL and Date being represented year to date.

• The chart DAI Circulating Supply and UST depegging is taken from the tables udm_events with UST price being taken from token price hourly. In order to figure out the circulating supply of DAI i found the running total of all tokens DAI was minted from the wallet, '0x0000000000000000000000000000000000000000' and the running total of DAI paid to the wallet '0x0000000000000000000000000000000000000000' and took them away from each other. Data is taken from April to the end of May.

• The chart DAI Circulating Supply and UST depegging is taken from the tables udm_events with UST price being taken from token_price_hourly. In order to figure out the circulating supply of DAI I found the running total of all tokens DAI was minted from the wallet, '0x0000000000000000000000000000000000000000' and the running total of DAI paid to the wallet '0x0000000000000000000000000000000000000000' and took them away from each other. Data is taken from April to the end of May.

• The chart DAI Repaid and UST depegging is taken from the tables 'udm_events' with UST price being taken from token_price_hourly. The sum of DAI paid to the wallet '0x0000000000000000000000000000000000000000' daily makes up Dai_repaid. Data is taken from April to the end of May.

Before the deppeging of UST, UST found itself in the top ten crypto currencies by marketcap, with Luna establishing itself as a top 10 crypto currency as well. With Luna outperforming most of the market at the start of the year. How did the wider crypto market respond to USTs fall from grace?

As you can see the arbitrage system worked relatively well when it came to maintaining the price of UST up until May. While the stablecoin was performing relatively well UST was seen by many as being one of the few stablecoins that could be viewed as being decentralised due to it relying on the market as opposed to reserves held by individuals, or held in the highly centralised USD. Unfortunately one of the things that made UST attractive also made it vulnerable to be exploited, as the arbitrage system could also be used to negatively impact the price.

Let's take a look at the stablecoins I mentioned in the introduction, and how they performed during the UST depegging.

The reputation of stablecoins maintaining their peg has led to their wild-scale use in crypto, with UST and USDT(to a lesser extent) falling below pegging in early May this had wider implications for crypto as a whole. There was a spike in crypto sent to exchanges with the majority being stablecoins and DEFI took a hit in terms of TVL, with it dropping by half. The stablecoin DAI's circulating supply dropped as billions was repaid by investors however this didn't have a negative impact on price due to MakerDaos over-collaterisation and the risk management implemented on the protocol. During this time period, Tether paid out over 10 billion from its reserves to USDT investors in USD. Interestingly BUSD, GUSD, TUSD, USDC and DAI all went above their pegging on the 12th of May, however, USDT with its dip below its pegging being smaller than BUSD's price increase above its pegging drew more attention.

Stablecoins max price during May was more volatile, with 3 stablecoins technically losing their pegging on the 12th of May. Notably, BUSD and GUSD were 4 cents above pegging and TUSD 2.5 cents above pegging, whereas USDT was 3 cents below on the minimum prices chart. However, this wasn't widely reported on, with a stablecoin being above its pegging likely being viewed as less worrying than it being below.

There are a number of Tokenised Gold Stablecoins with Pax Gold(PAXG) and Tether Gold being the most well-known. They both look to be pegged to the current USD price of Gold.

Pax Gold(PAXG) describes itself as 'a digitized version of real, physical gold of the highest quality: London Bullion Market Association-accredited London Good Delivery gold bars held in the most secure vaults in the world.'. It's backed one-to-one with gold and can be redeemed for physical gold globally, or for the USD based on the current price of Gold.

Tether Gold(XAUt) is also backed one-to-one with physical gold, however, they don't offer globally delivery or redemption of the Gold the asset is backed by globally, requiring investors to be in Switzerland. You can see the serial number of the physical Gold associated with your token on their website.

PAXG has an increased number of transactions indicating that it is the preferred stable coin, while the number of PAXG transactions is more likely to be in the hundreds, the number of transactions of XAUt are more likely to be under 30. The average price of each asset is relatively close although it is different indicating a difference in how both assets achieve pegging.

While I won't be exploring tokenised assets such as Gold in the rest of the dashboard, it's worth noting that stable coins are not just limited to fiat with there also being a number of tokenised stocks with the aim of maintaining a pegging to the associated stock on the stock market.

Tweet and accompanying image from Twitter thread detailing DAI collaterisation.

Additionally, a large part of the MakerDAO strategy is risk management, a risk team analyses a number of risks to manage related to the platform, creating risk models and figuring out ways to compensate for them. One way the Risk Team manage higher risk due to increased demand is through a variable stability fee on vaults in order to maintain a surplus supply of DAI. MakerDAO is an important example of how to better manage the risks associated with the volatility of crypto markets.