Frax Finance and osmosis

The world’s first fractional stablecoin and crypto native consumer price index Date of analysis : 26/02/2023

Net of deposit

> What does net of deposit mean? > > Net Deposits are the difference between the Total Deposits and Total Withdrawals you've made for a particular payment method - such as a debit or credit card. The Net Deposit figure is worked out simply by taking the Total Withdrawals amount from the Total Deposits amount.

> The term "net of deposit" in the context of crypto typically refers to the amount of cryptocurrency that remains in a wallet or account after deducting any deposits or withdrawals. > > For example, if someone has a crypto wallet with a balance of 10 BTC and they deposit 2 BTC, the net of deposit would be 12 BTC. Conversely, if they then withdrew 1 BTC, the net of deposit would be 11 BTC. > > This term can be useful for tracking changes in the amount of cryptocurrency held in a particular wallet or account, and can help to provide a clearer picture of the overall balance.

Average liquidity of each pool

In consecutive years, STARS/OSMO has had the highest amount of liquidity (about stars)

> What is stargaze zone? Stargaze is a zone in the Cosmos ecosystem that exemplifies high levels of security, decentralization, transparency, and flexibility. Stargaze is designed as a Proof-of-Stake Cosmos zone from the beginning, providing it the greatest flexibility in terms of protocol design, compatibility, and scalability.

summary and Conclusion

Ending thoughts & a functional way to visualize the Frax Protocol

Frax uses ideas from Uniswap and AMMs to build a novel hybrid stablecoin design never seen before. In a Uniswap pool, the ratio of asset A and B has to be proportional due to the constant product function. The LP token is just a pro rata claim on the pool + fees so it is usually increasing in value (if fees higher than impermanent loss) or loses value (if impermanent loss greater than fees). The LP token is just passive claims on the pool.

Frax takes that idea and turns it over to design a unique stablecoin. The LP token is the stablecoin, FRAX. It is the object of stabilization and always mintable/redeemable for $1 worth of collateral and the governance (FXS) token at the collateral ratio. This ratio of the two assets (collateral and FXS) dynamically changes based on the price of the stablecoin. If the stablecoin price is dropping, then the protocol tips the ratio in favor of collateral and less in the FXS token to regain confidence in FRAX. An arbitrage opportunity arises for people wanting to put in collateral into the pool at the new ratio for discounted FXS which the protocol mints for this "recollateralization swap." This recollateralizes the protocol to the new, higher collateral ratio.

If FRAX is over $1, then the protocol tips the collateral ratio to the FXS token to measure the market's confidence in more FRAX supply being stabilized algorithmically. As FRAX becomes more algorithmic, the excess collateral can go back to FXS holders through a buyback shares function that anyone can call to burn their FXS tokens for an equal value of excess collateral. The "buyback swap" function always keeps value accruing to the governance token any time there is excess fees/collateral/value in the system.

This 'Frax dance' is always happening and uses AMM game theory to test different ratios of collateralization, incentivize recollateralizing through arbitrage swaps, and redistribute excess value back to FXS holders through a buyback swap. The protocol starts at a 100% collateral ratio at genesis and might or might not ever get to purely algorithmic. The novel insight is to use market forces itself to see how much of a stablecoin can be algorithmically stabilized with its own seigniorage token so that it keeps a tight band around $1 like fiatcoins. Purely algorithmic/rebase designs like Basis, ESD, and Seigniorage Shares have wildly fluctuating prices as much as +-40% around $1 that take days/weeks to stabilize before going through another cycle. This is counterproductive and assumes the market actually wants/needs a stablecoin with 0% collateralization. Frax doesn't make this assumption. Instead, it measures the market's preference and finds the actual collateral ratio which holds a stablecoin tightly around $1, periodically testing small differences in the ratio when the price of FRAX slightly rises/drops. Frax uses AMM concepts to make a real-time fractional-algorithmic stablecoin that is as fast at price recovery as Uniswap is at keeping trading pools correctly priced. As this system gets more efficient and the velocity of the system increases, collateral pools can include other assets instead of stablecoins like volatile crypto such as ETH and wrapped BTC. As the price of the volatile asset rises, users will use the buy back shares function to distribute the excess value to FXS holders. When the price of the volatile collateral drops, there is an instant arbitrage opportunity to put in more crypto for discounted FXS to keep the collateral ratio at the target. Just like a Uniswap trading pair keeps its constant product function balanced, the Frax Protocol keeps its target collateral ratio balanced to what the market needs for FRAX to be $1.

The above example uses "collateral" and "FXS" as the two assets within the protocol, but in reality, Frax can have multiple pools of collateral and multiple algorithmic token pools with weights, similar to Balancer. The protocol currently has USDC collateral pools and just 1 algorithmic token: FXS. In v2, we will release a second algorithmic token, the Frax Bond token (FXB) which represents pure debt with an interest rate attached.

We believe that the fractional-algorithmic design of Frax is paradigm shifting for stablecoins. It is fast, real-time balancing, algorithmic, governance-minimized, and extremely resilient. We strongly believe the Frax protocol can become a foil to Bitcoin's "hard money" narrative by demonstrating algorithmic monetary policy to create a trustless stablecoin that all of the crypto community can embrace

analyst : : Drsimon

DISCORD :: hony.forto#9895

Volume and percentage of Deposit and Withdrawal of each pool

> The following charts are provided for better understanding and do not need additional explanations (everything is clear :/)

Number and percentage of delegators and validators of each pool

> The following charts are provided for better understanding and do not need additional explanations (everything is clear :/)

Deposits of each pool

- In consecutive years, ATOM/OSMO has had the largest deposit volume (about atom)

- In 2021 AKT/OSMO and JUNO/OSMO after the atom had the highest volume of deposits (about akt and juno)

- In 2022, USDC/OSMO and WETH/OSMO have the largest deposit volume after Atom (about usdc and weth)

- In 2023, WETH/OSMO and USDC/OSMO have the largest deposit volume after Atom (about usdc and weth)

> The suspicious volume was related to ATOM/OSMO and JUNO/OSMO : October 3, 2021

Deposits and withdrawals

The following charts show all deposits and withdrawals of osmosis in Frax Finance

According to the annual chart, the highest deposit amount is in 2021 and the highest withdrawal amount is in 2022

> Deposits and withdrawals in crypto refer to the process of transferring cryptocurrencies into and out of a cryptocurrency exchange or wallet. This process allows users to buy, sell, and trade cryptocurrencies and also to store their cryptocurrencies in a secure location. > > To make a deposit in crypto, the user needs to have a cryptocurrency wallet address provided by the exchange or wallet service. The user can then transfer cryptocurrencies from their personal wallet to this address by sending the correct amount of cryptocurrency to the address provided. The deposit will usually be confirmed after a certain number of blockchain confirmations, depending on the cryptocurrency being transferred. > > To make a withdrawal in crypto, the user needs to initiate a withdrawal request through the exchange or wallet service. The user will need to provide the destination wallet address and the amount of cryptocurrency they wish to withdraw. The exchange or wallet service will then process the withdrawal and transfer the requested amount of cryptocurrency to the provided wallet address. The withdrawal may take a certain amount of time to be processed and confirmed on the blockchain, depending on the cryptocurrency being withdrawn and the processing speed of the exchange or wallet service. > > It is important to note that cryptocurrency transactions are irreversible, meaning that once a transaction is confirmed on the blockchain, it cannot be cancelled or reversed. Therefore, users should take care to ensure that they are sending the correct amount of cryptocurrency to the correct wallet address when making deposits and withdrawals.

Number of delegators

> What is a delegator in crypto? > > Delegators are token holders who cannot, or do not want to run a validator node themselves. Instead, they secure the network by delegating their stake to validator nodes and play a critical role in the system, as they are responsible for choosing validators.

- According to the charts below, atom/osmo has the most delegators

- In 2022, Atom/Osmo had over than 77 thousand delegates

- In 2023 until today (atom/osmo) has had nearly 5 thousand delegates

> In the context of cryptocurrency, a delegator refers to an individual or entity that delegates their cryptocurrency holdings to a validator or node operator on a proof-of-stake (PoS) blockchain network. > > In a PoS blockchain network, validators are responsible for validating transactions and adding new blocks to the blockchain. They are rewarded with transaction fees and newly minted cryptocurrency for their work. However, in order to become a validator, one must first stake a certain amount of cryptocurrency as collateral. > > This is where delegators come in. Rather than staking their own cryptocurrency to become a validator, delegators can delegate their cryptocurrency to a validator or node operator, who will then use it as collateral to become a validator. In exchange, the delegator receives a portion of the validator's rewards, proportional to the amount of cryptocurrency they delegated. > > Delegating allows individuals to participate in the validation process and earn rewards without the technical expertise and infrastructure required to become a validator themselves. It also helps to decentralize the network by distributing the responsibility of validation across multiple validators and node operators.

Number of validators

> What are crypto validators? > > With regard to blockchains such as Bitcoin and Ethereum (until September 2022) that use a proof-of-work (PoW) consensus mechanism, validators are computers dedicated to maintaining a blockchain's integrity. Validator nodes may store the full blockchain or an abbreviated version that is quicker to analyze.

- Through the charts below, you can check and compare the validators of different pools

- atom/osmo had 183 validators in 2022 :upside_down_face:

Accumulation of the volume of each pool

The following charts show the accumulation of transaction volume in different time frames

CRO/OSMO have the highest transactions volume to date

> CRO and OSMO are two different cryptocurrencies that operate on separate blockchain networks. CRO is the native cryptocurrency of the Crypto.com blockchain, while OSMO is the native cryptocurrency of the Osmosis blockchain. > > Transactions involving CRO and OSMO are typically conducted on their respective blockchain networks. To initiate a transaction, you would need to have a wallet that supports the specific cryptocurrency you wish to transact with. You would then need to send the cryptocurrency to the recipient's wallet address using the appropriate transaction fee and gas fee (if applicable) for the network. > > It's important to note that cryptocurrency transactions can be irreversible and carry some degree of risk, so it's important to take appropriate precautions and conduct due diligence before engaging in any cryptocurrency transactions.

Total and percentage of transactions volume of each pool

> The following charts are provided for better understanding and do not need additional explanations (everything is clear :/)

Total and percentage of transactions of each pool

The following charts are provided for better understanding and do not need additional explanations (everything is clear :/)

Volume of pools

The volume of the cro/osmo pool is much larger than other pools

You can see the heavy transactions of this pool in the daily time frame

In 2022, the volume of this pool was close to 2 billion Also, in 2023 until today, the transaction volume of this pool has been more than 106 million

Accumulation of transactions of each pool

The following charts show the accumulation of the number of transactions in different time frames

ATOM/OSMO have the highest number of transactions to date

> ATOM and OSMO are two different cryptocurrencies that use different blockchain technologies. ATOM is based on the Cosmos network, while OSMO is based on the Cosmos SDK. Both of these cryptocurrencies allow for transactions to be made between parties, but they have some differences in how their pools and transactions work. > > In the Cosmos network, the ATOM token is used as a staking token to secure the network and validate transactions. Users can stake their ATOM tokens to become a validator or delegate their tokens to a validator to earn rewards. The staking process also allows for the creation of new blocks and the validation of transactions. The ATOM pool is the pool of staked tokens that are used for network security. > > On the other hand, the OSMO token is used as the native currency for the Osmosis network, which is a decentralized exchange (DEX) that runs on top of the Cosmos SDK. In the Osmosis network, liquidity providers can add tokens to liquidity pools to earn fees on trades made through the DEX. The OSMO pool is the pool of tokens that are added to the liquidity pool and used for trading on the DEX. > > When it comes to transactions, both networks use a similar process. Transactions are initiated by a user who creates and signs a transaction using their private key. The transaction is then broadcast to the network, where it is validated by a series of nodes before being added to the blockchain. Once the transaction is confirmed, the user's account balance is updated to reflect the transaction. > > Overall, while both ATOM and OSMO allow for transactions to be made, they have different use cases and functions within their respective blockchain networks. ATOM is primarily used for staking and securing the network, while OSMO is used for trading on a decentralized exchange.

Namber of transctions of each pool

The charts below show the number of transactions in each pool According to the annual graph, the Atom/Osmo pool had the highest transaction volume in 2022 The number of transactions in this pool was nearly 270 thousand

In the new year, this pool (atom/osmo) had the highest amount of transactions The number of transactions in this pool has been close to 13 thousand

LP Actions

> What is LP Actions in Crypto? > > LP Actions, also known as Liquidity Provider Actions, in crypto refer to the activities undertaken by individuals or entities who provide liquidity to decentralized exchanges (DEXs) through liquidity pools. > > In a decentralized exchange, there are no centralized entities to provide liquidity. Instead, liquidity is provided by users who deposit their cryptocurrency assets into a liquidity pool. These assets are used to facilitate trading on the DEX and are rewarded with trading fees. In return for their participation, liquidity providers receive a share of the trading fees generated by the pool. > > LP Actions refer to the various activities that liquidity providers can undertake to optimize their rewards and minimize their risks. For example, LPs may adjust the ratio of assets they have deposited into a pool, to account for fluctuations in the market. They may also take action to protect their investments during periods of high volatility or when there are sudden market movements. > > Other LP Actions can include strategies such as impermanent loss protection or yield farming, where LPs deposit tokens into different pools to maximize their returns. Overall, LP Actions are an important consideration for those looking to participate in liquidity provision on DEXs, as they can greatly impact the profitability and risk associated with such investments.

According to the charts of Unique liquidity providers, you can understand how similar these charts are to the charts of LP actions

So, when Unique liquidity providers have increased, LP actions have also increased and vice versa.

New users in new year

> The chart below shows new FRAX users who made their first transaction on osmo in the new year

FTX and Transfers

Liquidity providers and LP actions

Total and Percentage of incoming/outgoing transfers

> The following charts are provided for better understanding and do not need additional explanations (everything is clear :/)

Number of incoming/outgoing transfers

> The following charts are provided for better understanding and do not need additional explanations (everything is clear :/)

Introduction

Frax Finance is a decentralized stablecoin project that aims to provide a stable and scalable currency for use in the decentralized finance (DeFi) ecosystem. The Frax stablecoin is designed to maintain its value at $1, and it achieves this through a unique algorithmic mechanism that adjusts the coin's supply based on market demand. Frax is backed by a combination of collateral and algorithmic mechanisms that aim to maintain the price stability of the stablecoin.

Frax Finance was created by Sam Kazemian and Travis Moore, who launched the project in December 2020. The project has since gained popularity in the DeFi space, and its stablecoin is now available on several decentralized exchanges (DEXs) like Uniswap and SushiSwap.

One of the unique aspects of Frax Finance is that it uses a dual-currency system, with both a stablecoin (FRAX) and a governance token (FXS). The FXS token is used to incentivize users to hold and stake the token, as well as to participate in governance decisions related to the Frax protocol.

Overall, Frax Finance aims to provide a stable, decentralized currency that can be used in a variety of DeFi applications. The project has gained significant traction in the DeFi space and is seen as a promising player in the growing stablecoin market.

Methodology

-

Introduction

-

Frax Finance Stablecoin Protocol

-

Frax Shares (FXS)

-

Price Stability

-

Collateral Ratio

-

TOP NEWS

-

What is the relationship between Frax Finance and osmosis network?

-

Top tokens - Daily price

\

- Transactions and volumes

-

Total volume and transactions and their accumulation

-

Namber of transctions of each pool

-

Accumulation of transactions of each pool

-

Total and percentage of transactions of each pool

-

Volume of pools

-

Accumulation of the volume of each pool

-

Total and percentage of transactions volume of each pool

\

-

- Transactions and volumes

-

Validators and Delegators

-

Number of validators

-

Number of delegators

-

Number and percentage of delegators and validators of each pool

\

-

-

Deposits and withdrawals

-

Deposits and withdrawals of pools

-

Deposits of each pool

-

Withdrawals of each pool

-

Volume and percentage of Deposit and Withdrawal of each pool

-

Net of deposit Average

-

Liquidity of each pool

\

-

-

FTX and Transfers

-

The impact of FTX news on transfers

-

Number of Incoming transfers

-

Number of outgoing transfers

-

Number of incoming/outgoing transfers

-

Total and Percentage of incoming/outgoing transfers

\

-

-

Liquidity providers and LP actions

- Unique liquidity providers

- LP Actions

-

New users in new year

-

summary and Conclusion

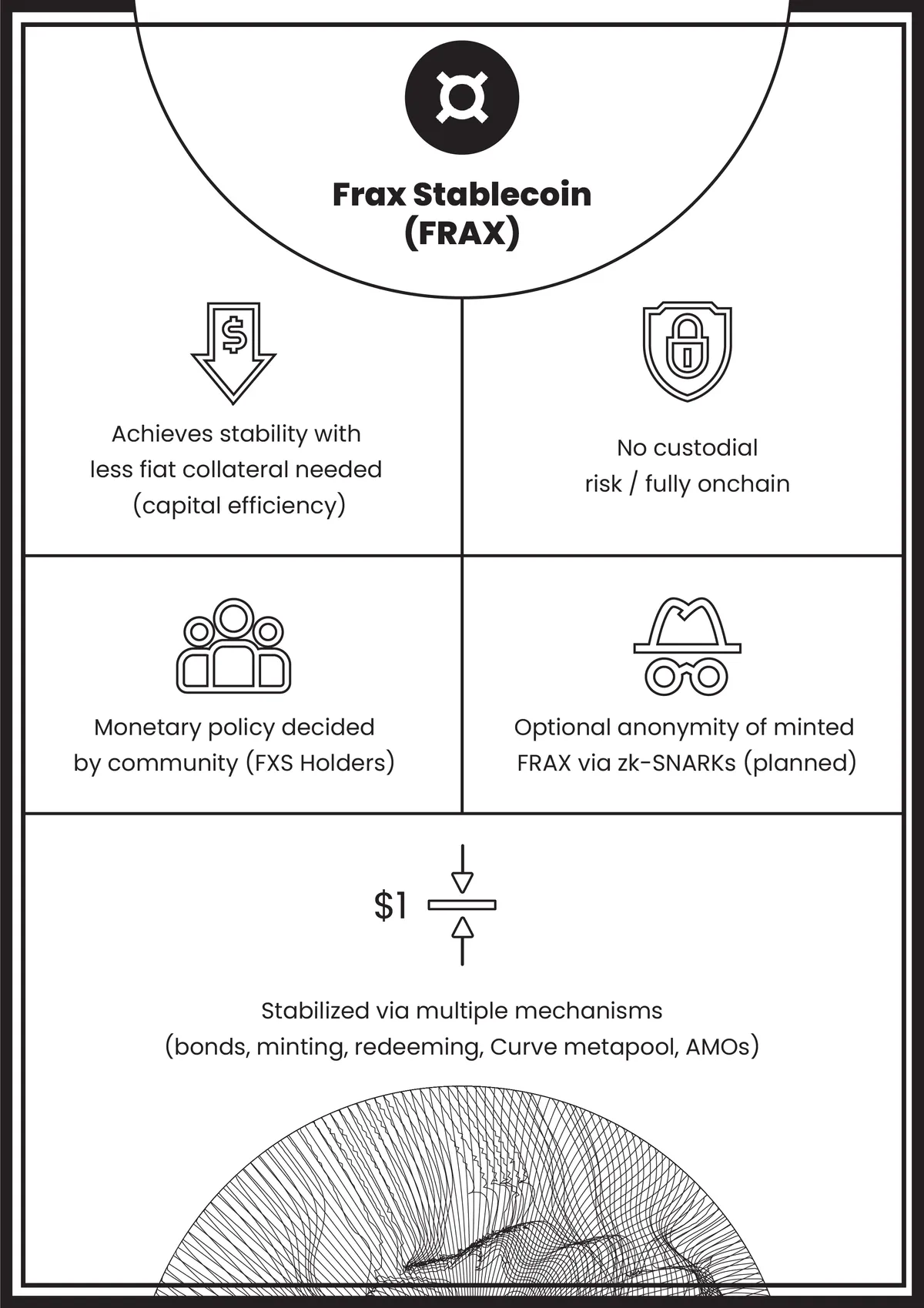

Frax Finance Stablecoin Protocol

The Frax Protocol issues innovative, decentralized stablecoins and contains subprotocols to support them. The Frax Protocol currently issues 3 stablecoins: FRAX, FPI, and frxETH. The Frax Protocol also has 3 subprotocols within it that integrate its stablecoins: Fraxlend, Fraxswap, and Fraxferry.

Core concepts to understand the unified Frax Finance ecosystem include:

- Three Stablecoins – The Frax Protocol currently issues 3 stablecoins. FRAX, a USD pegged asset. The Frax Price Index (FPI) stablecoin, the first stablecoin pegged to a basket of consumer goods creating its own unit of account separate from any nation state denominated money. FraxEther (frxETH), pegged to ETH for use as a replacement for WETH in smart contracts.

- Fraxswap, a native AMM – Fraxswap is the first AMM with time weighted average market maker orders used by the Frax Protocol for rebalancing collateral, mints/redemptions, expanding/contracting stablecoin supply, and deploying protocol owned liquidity onchain.

- Fraxlend, permissionless lending markets – Fraxlend is the lending facility for Frax-based stablecoins allowing debt origination, customized non-custodial loans, and onboarding collateral assets to the Frax Finance economy.

- Fraxferry, optimistic transfer protocol for Frax-based tokens – Fraxferry transfers natively issued Frax Protocol tokens across many blockchains.

- Frax Share (FXS) as base layer governance token – Frax Share (FXS) is the governance token of the entire Frax ecosystem of smart contracts which accrues fees, revenue, and excess collateral value. FPIS is the governance token of FPI only and splits its value capture with FXS holders.

- Gauge Rewards System – The community can propose new gauge rewards for strategies that integrate Frax-based stablecoins. FXS emissions are fixed, halve each year, and entirely flow to different gauges based on the votes of veFXS stakers.

Website: https://app.[frax.finance](https://frax.finance) Telegram: Telegram (announcements / news): Twitter: Medium / Blog: Governance (discussion): Governance (voting):

Price Stability

How arbitrage keeps FRAX price-stable?

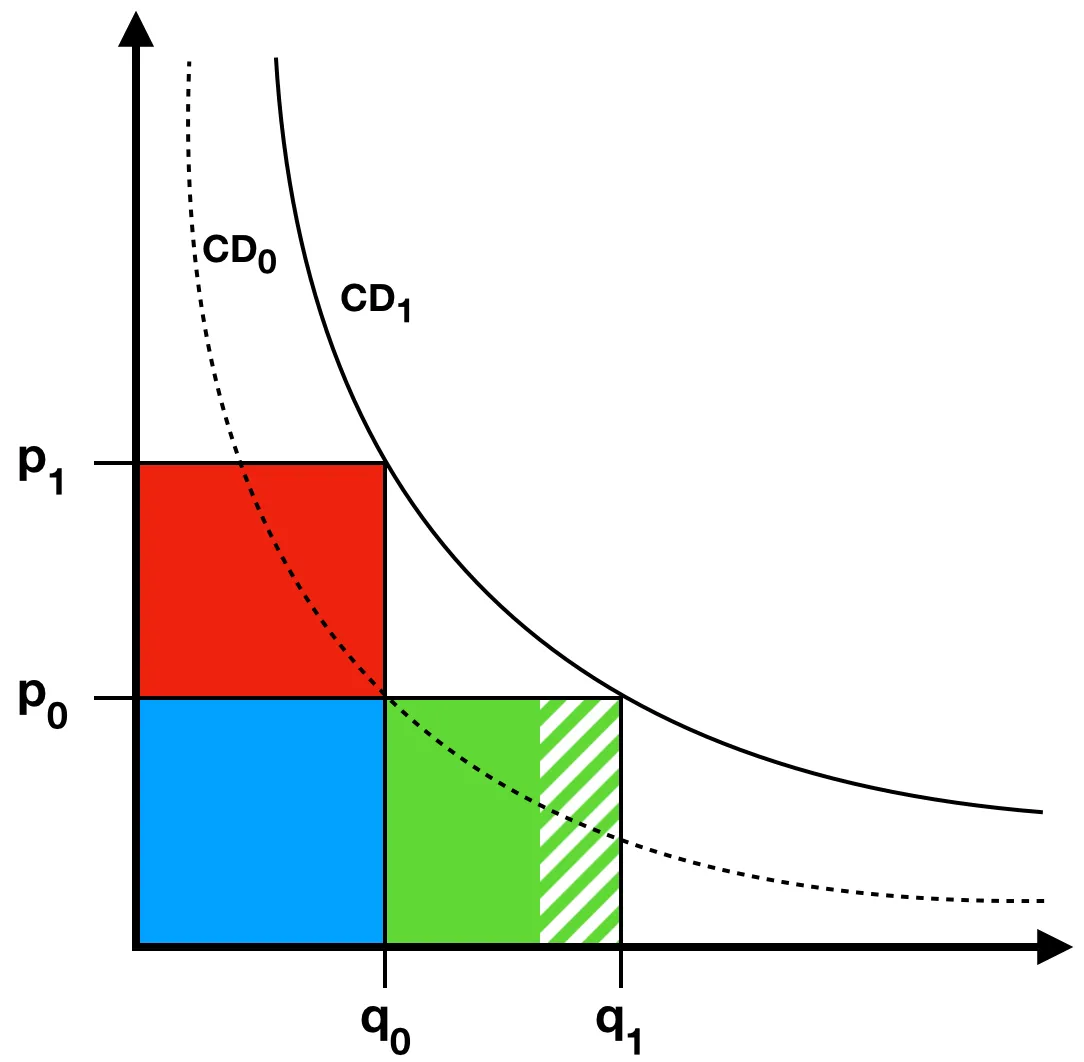

FRAX can be minted and redeemed from the system for $1 of value, allowing arbitragers to balance the demand and supply of FRAX in the open market. At all times in order to mint new FRAX a user must place $1 worth of value into the system. If the market price is above the price target of $1, then there is an arbitrage opportunity to mint tokens by placing $1 of value into the system per FRAX and sell the minted FRAX for above $1 in the open market. The difference is simply the proportion of FXS and collateral comprising the $1 of value. When FRAX is in the 100% collateral phase, all of the value that is used to mint FRAX is collateral. As the protocol moves into the fractional state, some of the value that enters into the system during minting becomes FXS (which is then burned). For example, in a 96% collateral ratio, every FRAX minted requires $.96 of collateral and burning $.04 of FXS. In a 95% collateral ratio, every FRAX minted requires $.95 of collateral and burning $.05 of FXS, and so on.

If the market price of FRAX is below the price range of $1, then there is an arbitrage opportunity to redeem FRAX tokens by purchasing cheaply on the open market and redeeming FRAX for $1 of value from the system. At all times, a user is able to redeem FRAX for $1 worth of value from the system. The difference is simply what proportion of the collateral and FXS is returned to the redeemer. When FRAX is in the 100% collateral phase, 100% of the value returned from redeeming FRAX is collateral. As the protocol moves into the fractional phase, part of the value that leaves the system during redemption becomes FXS (which is minted to give to the redeeming user). For example, in a 98% collateral ratio, every FRAX can be redeemed for $.98 of collateral and $.02 of minted FXS. In a 97% collateral ratio, every FRAX can be redeemed for $.97 of collateral and $.03 of minted FXS.

The FRAX redemption process is easy to understand and economically sound. During the 100% phase, it is trivially simple. During the fractional/algorithmic phase, FXS is burned as FRAX is minted. On the other hand, when FRAX is redeemed, minting of FXS occurs. When there is demand for FRAX, redeeming it for FXS plus collateral initiates minting of a similar amount of FRAX into circulation on the other end (which burns a similar amount of FXS). The value that accrues to the FXS market cap is the sum of the non-collateralized value of FRAX’s market cap. FXS token’s value is therefore partially determined by the demand for FRAX. This is the summation of all past and future shaded areas under the curve displayed as follows.Frax Finance Stablecoin Protocol

Collateral Ratio

The protocol adjusts the collateral ratio during times of FRAX expansion and retraction. During times of expansion, the protocol decollateralizes (lowers the ratio) the system so that less collateral and more FXS must be deposited to mint FRAX. This lowers the amount of collateral backing all FRAX. During times of retraction, the protocol recollateralizes (increases the ratio). This increases the ratio of collateral in the system as a proportion of FRAX supply, increasing market confidence in FRAX as its backing increases.

At genesis, the protocol adjusts the collateral ratio once every hour by a step of .25%. When FRAX is at or above $1, the function lowers the collateral ratio by one step per hour and when the price of FRAX is below $1, the function increases the collateral ratio by one step per hour. This means that if FRAX price is at or over $1 a majority of the time through some time frame, then the net movement of the collateral ratio is decreasing. If FRAX price is under $1 a majority of the time, then the collateral ratio is increasing toward 100% on average.

In a future protocol update, the price feeds for collateral can be deprecated and the minting process can be moved to an auction based system to limit reliance on price data and further decentralize the protocol. In such an update, the protocol would run with no price data required for any asset including FRAX and FXS. Minting and redemptions would happen through open auction blocks where bidders post the highest/lowest ratio of collateral plus FXS they are willing to mint/redeem FRAX for. This auction arrangement would lead to collateral price discovery from within the system itself and not require any price information via oracles. Another possible design instead of auctions could be using PID-controllers to provide arbitrage opportunities for minting and redeeming FRAX similar to how a Uniswap trading pair incentivizes pool assets to keep a constant ratio that converges to their open market target price.

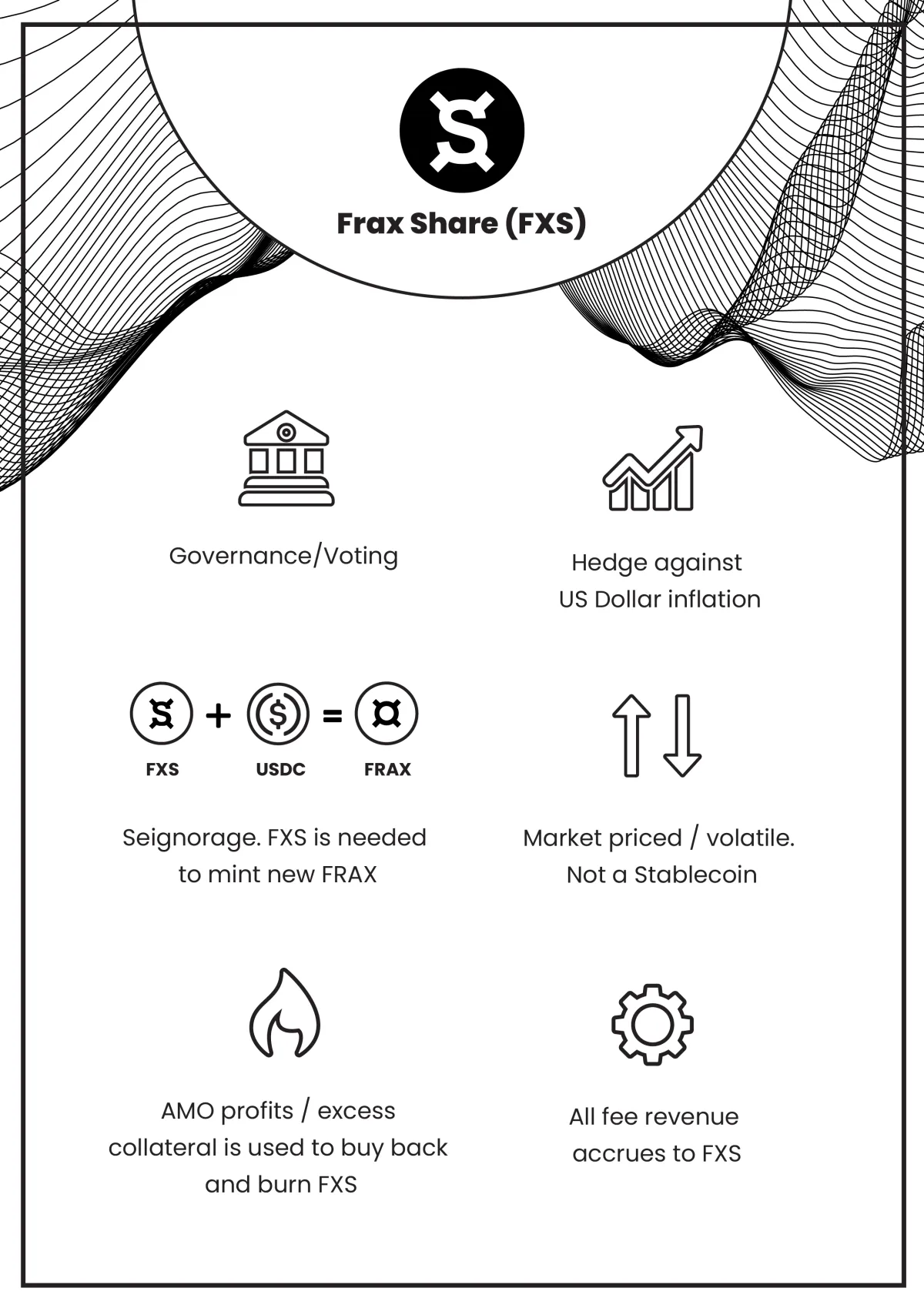

Frax Shares (FXS)

FXS is the value accrual and governance token of the entire Frax ecosystem. All utility is concentrated into FXS.

The Frax Share token (FXS) is the non-stable, utility token in the protocol. It is meant to be volatile and hold rights to governance and all utility of the system. It is important to note that we take a highly governance-minimized approach to designing trustless money in the same ethos as Bitcoin. We eschew DAO-like active management such as MakerDAO. The less parameters for a community to be able to actively manage, the less there is to disagree on. Parameters that are up for governance through FXS include adding/adjusting collateral pools, adjusting various fees (like minting or redeeming), and refreshing the rate of the collateral ratio. No other actions such as active management of collateral or addition of human-modifiable parameters are possible other than a hardfork that would require voluntarily moving to a new implementation entirely. The FXS token has the potential of upside utility and downside utility of the system, where the delta changes in value are always stabilized away from the FRAX token itself. FXS supply is initially set to 100 million tokens at genesis, but the amount in circulation will likely be deflationary as FRAX is minted at higher algorithmic ratios. The design of the protocol is such that FXS would be largely deflationary in supply as long as FRAX demand grows.

The FXS token’s market capitalization should be calculated as the future expected net value creation from seigniorage of FRAX tokens in perpetuity, the cash flow from minting and redemption fees, and utilization of unused collateral. Additionally, as the market cap of FXS increases, so does the system’s ability to keep FRAX stable. Thus, the priority in the design is to accrue maximal value to the FXS token while maintaining FRAX as a stable currency. As Robert Sam’s described in the original Seigniorage Shares whitepaper: “Share tokens are like the asset side of a central bank’s balance sheet. The market capitalisation of shares at any point in time fixes the upper limit on how much the coin supply can be reduced.” Likewise, the Frax protocol takes inspiration from Sams’ proposal as Frax is a hybrid (fractional) seigniorage shares model.

veFXS & Long Term Staking

In May 2020, the protocol now allows FXS holders to lock up FXS tokens to generate veFXS and earn special boosts, special governance rights, and AMO profits. Check the in depth veFXS specs for more information on how all veFXS features function.

What is the relationship between Frax Finance and osmosis network?

Frax Finance and Osmosis Network are both decentralized finance (DeFi) projects built on top of the Cosmos SDK blockchain platform, but they have different focuses and operate independently of each other.

Frax Finance is a stablecoin protocol designed to provide a stable and decentralized currency that is backed by a combination of collateralized stablecoins, crypto assets, and algorithmic mechanisms. It aims to maintain a stable price of around $1 USD per Frax token, while also providing users with the ability to earn yields by staking their tokens or providing liquidity to Frax pools. Frax Finance is built on top of the Ethereum blockchain, and it is also available on other blockchain networks like Binance Smart Chain and Polygon.

Osmosis Network, on the other hand, is a decentralized exchange (DEX) built on the Cosmos SDK that enables users to trade a wide variety of assets on its platform. It uses an automated market maker (AMM) mechanism, which means that it does not rely on order books but instead uses liquidity pools to determine the prices of assets. Osmosis Network also allows users to earn rewards by providing liquidity to its pools, which are denominated in its native token, OSMO.

While Frax Finance and Osmosis Network share some similarities, they are fundamentally different projects with different goals and functions. Frax Finance focuses on providing a stablecoin that is decentralized and can be used as a medium of exchange, while Osmosis Network is focused on providing a decentralized exchange platform for trading various assets.

Top tokens - Daily price

The chart below shows the average daily price of the tokens mentioned above

> Note that the prices are in USD

TOP NEWS

The community of Frax Finance, a decentralized finance protocol with some $2 billion in total value locked, voted to fully collateralize the protocol’s native stablecoin frax (FRX), according to a vote concluded Wednesday. Proposal FIP-188, posted last week on Frax’s governance forum, suggested setting the target collateral ratio to 100% using protocol earnings to increase the stablecoin reserves. The result represents a significant shift for FRX, the fifth-largest stablecoin with more than $1 billion in market capitalization, as it eliminates the algorithmic element of the stablecoin’s stabilizing mechanism.

Frax uses a hybrid design to keep its price pegged to the U.S. dollar. It is 80% backed by crypto asset collateral and partially stabilized algorithmically, burning and minting the protocol’s governance token FXS. Its issuer, Frax Finance, is managed by a decentralized autonomous organization through community proposals and votings. According to the proposal, the protocol will not create additional FXS to hike the collateral ratio, which would inflate the token’s supply. Instead, it proposes retaining protocol revenues and authorizing the purchase of up to $3 million of frxETH, the protocol’s liquid ether staking derivative, to prop up reserves. Sam Kazemian, co-founder of Frax Finance, said in the project's Telegram group chat that he favored increasing the collateral for being the "safest design, while also being the most capital efficient." Some 98% of the voters favored the proposal. Frax’s decision comes after multiple algorithmic stablecoins lost their price peg and eventually collapsed last year, triggering a wider downfall in crypto markets. The highest-profile fall, terraUSD’s death spiral in May, wiped out several digital asset firms in the subsequent contagion.

Frax has been the fastest-growing liquid staking protocol for ETH with a 42% growth over the past 30 days, according to data by DefiLlama.

DISCLAIMER: Not Investment Advice

The information provided is for general information purposes only. No information, materials, services and other content provided on this page constitute solicitation, recommendation, endorsement or any financial, investment, or other advice. Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decision.

> Please note that all the charts below are made in multi-time frames.

Transactions and volumes

Total volume and transactions and their accumulation

In the charts below, the number of Osmise network transactions and the volume of transactions are shown In 2022, more than 720 thousand transactions have been recorded for this network in Frax Finance And in the new year, more than 55 thousand transactions have been registered so far

The volume of transactions in 2022 was more than 2.5 billion And in the new year more than 157 million

Validators and Delegators

Deposits and withdrawals

Withdrawals of each pool

- In consecutive years, ATOM/OSMO has had the largest Withdrawal volume (about atom)

- In 2021 AKT/OSMO and JUNO/OSMO after the atom had the highest volume of Withdrawal (about akt and juno)

- In 2022, USDC/OSMO and JUNO/OSMO and WETH/OSMO have the largest Withdrawal volume after Atom (about usdc and weth)

- In 2023, USDC/OSMO and WETH/OSMO WBTC/OSMO and EVMOS/OSMO have the largest Withdrawal volume after Atom (about wbtc)

> The suspicious volume was related to ATOM/OSMO and JUNO/OSMO : October 3, 2021

The impact of FTX news on transfers

Why did the FTX collapse?

FTX and FTX.US crashed due to a lack of liquidity and mismanagement of funds, followed by a large volume of withdrawals from rattled investors. The value of FTT plummeted, taking other coins down with it including Ethereum and Bitcoin, which reached a two-year low as of Nov 9.

What happened between FTX and Binance?

FTX in November 2022 faced a liquidity crisis and searched for bailout funds; rival exchange Binance considered buying portions of the company but quickly backed out. By Nov. 11, 2022, FTX's CEO stepped down and the company filed for bankruptcy.

binance said it will sell all its FTT tokens

Binance, the world’s biggest crypto exchange, announced on Nov. 6 that it would sell its entire position in FTT tokens—roughly 23 million FTT tokens valued at about $529 million. Binance CEO Changpeng “CZ” Zhao said the decision to liquidate the exchange’s FTT position was based on risk management, following the collapse of the Terra (LUNA) crypto token earlier in 2022.

> In early November, just days before the cryptocurrency exchange FTX filed for bankruptcy, its founder, Sam Bankman-Fried, reached out to his archrival, Changpeng Zhao, to ask for help. > > “I don’t know how things got so bad between us,” Mr. Bankman-Fried texted Mr. Zhao, according to a person with knowledge of the exchange. “I need your help for the sake of the industry and users.” > > Mr. Zhao, the founder of Binance, the world’s largest cryptocurrency exchange, initially agreed to provide a loan and buy FTX to save it. But after examining FTX’s books — and seeing the extent of its financial troubles — Mr. Zhao changed his mind, and Mr. Bankman-Fried had no choice but to put his company into bankruptcy. On Monday, Mr. Bankman-Fried was arrested in the Bahamas after American prosecutors filed criminal charges against him. > > Mr. Zhao’s actions were the culmination of a complicated relationship between the founders of the two biggest cryptocurrency exchanges, one that has sometimes involved the two men sparring publicly and taunting each other on Twitter. As the rapid growth of their companies turned both into paper billionaires, their competing visions of the cryptocurrency industry — and whether and how it should be regulated — held enormous sway, especially with governments around the world poised to crack down. > > \

Number of Incoming transfers

After the events of ftx and according to the charts below, it can be said that the number of incoming transfers has decreased

This incident shows the decrease of people's trust in the world of digital currencies

Of course, it should be noted that in 2022, more than 1 billion transfers received from the osmo network were made in Frax Finance.

Number of outgoing transfers

According to the charts below, it can be said that the number of outgoing transfers increased until some time after this news (about 2 weeks).

In 2022, less than 500,000 outgoing transfers of the osmo network have been in Frax Finance, which indicates the ratio of 1/2 of the outgoing transfers to the incoming transfers of this network.

Unique liquidity providers

> A liquidity provider is an individual or organization that supplies liquidity to a financial market, such as a stock exchange, forex market, or cryptocurrency exchange. Liquidity providers help ensure that there is always enough supply and demand in the market to facilitate trades and prevent prices from fluctuating too dramatically. > > In practice, a liquidity provider might offer to buy or sell a particular asset at a particular price, creating a "liquidity pool" that other traders can access. By doing so, the liquidity provider helps ensure that there is always a market for that asset, even if there are no other buyers or sellers at the moment. > > Liquidity providers can be banks, market makers, or other financial institutions that have the resources and expertise to offer large volumes of trading activity. They may earn profits through the bid-ask spread or through other fees charged to traders accessing their liquidity pools.

In the charts below, the number of liquidity providers for OSMO in Frax Finance is shown

March 1 2022 , has the largest number of liquidity providers

March 1 has the largest number of liquidity providers Since April 2022, the number of these people has decreased, and it can be said that people's confidence has decreased due to the Bitcoin dump and negative news at that time, in relation to the provision of liquidity.

Also, the number of liquidity providers has decreased a lot after the news of FTX, so that it has reached its lowest number in the last 1.5 years (as of August 2021).

> In the yearly chart, you should note that this number of people is unique and the numbers are completely correct

count(DISTINCT liquidity_provider_address) as "unique liquidity providers",