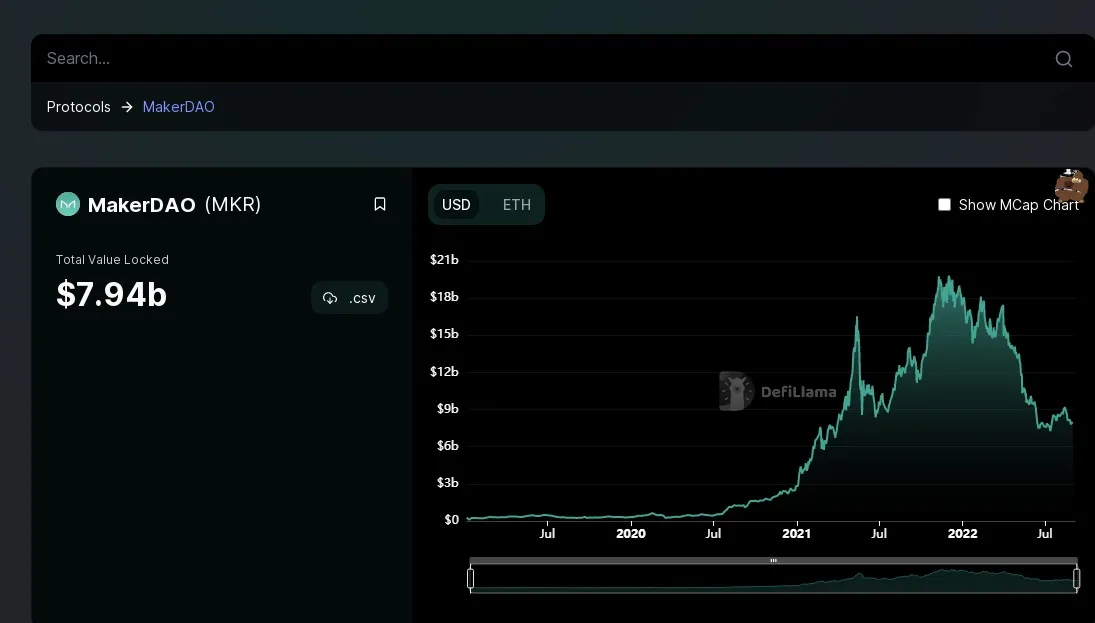

Open Analytics Bounty: MakerDao

Open analytics bounties are all about deep dive dashboards into one specific topic.

In Brief

- MakerDAO is a decentralized organization built on Ethereum to allow lending and borrowing of cryptocurrencies without the need for a middle man

- MakerDAO is made up of a smart contract service that manages borrowing and lending, as well as two currencies: DAI and MKR to regulate the value of loans.

- MakerDAO is a part of the "DeFi" movement - a catch-all term for financial tools and services that don't rely on centralized parties to coordinate and control access.

What is MakerDAO?

MakerDAO is an organization developing technology for borrowing, savings, and a stable cryptocurrency on the Ethereum blockchain. It has created a protocol allowing anyone with ETH and a MetaMask wallet to lend themselves money in the form of a stablecoin called DAI. By locking up some ETH in MakerDAO’s smart contracts, users can create a certain amount of DAI–the more ETH locked up, the more DAI can be created. When users are ready to unlock their ETH, which serves as collateral for their DAI loan, they simply pay back the loan along with any fees.

MakerDAO has created a core layer of the decentralized financial system on Ethereum–what the kids these days are calling “DeFi”.

Background of MakerDAO and How It Works?

The next significant highlight in an account of MakerDAO explained comprehensively would be the background of the protocol. You need to understand what exactly drove the origins of such a unique protocol. Interestingly, the decentralized lending platform is one of the first projects in the DeFi space. The platform’s founder, Rune Christensen, is currently the CEO of the platform. It also successfully garnered an investment of $15 million from venture capital firm Andreessen Horowitz in 2018. Where did all these start from?

The basic premise for introducing a platform like MakerDAO revolves around the approaches followed for lending and borrowing on blockchain. One would reasonably wonder how borrowing works on blockchain without any credit checks in a trustless environment. In such cases, the obvious answer often points towards liquidity, which implies the possibility of converting an asset into capital.

The protocol works by allowing anyone to take out loans in DAI using other cryptocurrencies as collateral. Crucially, these loans are overcollateralized, meaning that you will have to deposit more cryptocurrency than you put in. As of August 2022, the minimum collateralization rate of a “vault” of ETH is 170%, meaning that you would have to collateralize $170,000 worth of ETH to receive $100,000 worth of DAI.

The reason for overcollateralization is to protect against crashes of ETH or the other coins that back DAI, which include wrapped bitcoin (wBTC) and centralized U.S. dollar stablecoins USDC and USDP.

As of this writing in August 2022, DAI is backed by $10.6 billion worth of crypto assets and a smattering of real-world assets, such as $100 million from Huntington Valley Bank.

The MakerDAO crypto protocol introduced the benefit of liquidity in crypto lending and borrowing. For instance, when the collateral for a specific loan, i.e., ETH, has dropped in value by a considerable margin below the amount of the loan in DAI, the loan goes through liquidation. Therefore, the platform can sell off ETH collateral for paying loans borrowed in DAI alongside the fees and penalties. You can notice how liquidity and the threat of liquidation ensure stability in lending and borrowing on blockchain.

What motivates users to lock up more than they borrow?

The lender-borrower structure seems to be great for MakerDAO, but why would anyone want to borrow less than they lock up? The main reason is that by borrowing DAI (as opposed to buying it), an investor would be able to access a U.S. dollar stablecoin without having to sell his or her ETH. This is useful because many yield farms and lending platforms offer higher returns for U.S. dollar stablecoins than for ETH itself. DAI can be converted back to ETH at any time.

There’s also another token within MakerDAO’s network, which is MakerDAO’s governance token, Maker (MKR). The token is used primarily to vote on protocol updates within the platform. As of August 2022, MKR had a market capitalization of about $1.1 billion.

Then there’s the Dai Savings Rate (DSR), which is a savings protocol that issues returns to those who lock up DAI in the DSR’s smart contract. This lets those within Maker’s governance module influence the demand for DAI by changing the levers of the protocol’s monetary policy, just like a centralized bank.

So far, DAI’s done remarkably well, rising from a market capitalization of $100 million in early 2020 to a peak of $10 billion in February 2022, before falling to $6.4 billion in May 2022 after the crypto market crashed. As of August 2022, DAI’s market cap was $7.5 billion.

MakerDAO’s governance

Part of MakerDAO’s success isn't in its algorithmic design, but in its decentralized governance. Those with lots of MKR all but saved DAI from collapse in March 2020 after the pandemic shook the token to its core.

To prevent it from falling below $1, the decentralized autonomous organization voted to back the stablecoin with USDC, a centralized stablecoin maintained by Centre, a consortium led by payment company Circle and crypto exchange Coinbase. Since then, DAI has also added USDP to the mix. These stablecoins are distinctly centralized as they are run by companies and backed by USD and equivalents held in banks.

More generally, the governance protocol works to update the protocol through a series of time-based polls. These votes take place directly on the blockchain, and MKR tokens are the currency of the ballot. If a resolution passes, it’s binding.

Tokens of MakerDAO

Speaking of a Decentralized Autonomous Organization or DAO in identifying “how does MakerDAO work**,”** governance would emerge as a prominent highlight. What is the assurance of decentralization when the Maker Foundation exerts control over the Maker protocol? This is where you need to take note of the tokens on MakerDAO platform, i.e., DAI and MKR. Both the tokens are core components of the protocol and serve essential functionalities.

- DAI

First of all, you need to note that the DAI token is the stable cryptocurrency pegged against the US dollar. The operations of DAI depend considerably on supply and demand trends. It serves as the medium for facilitating loans against the collateral placed by borrowers on the platform.

- MKR

The MKR token, on the other hand, is an essential requirement in the MakerDAO crypto protocol for providing liquidity. With the help of MKR token, the platform can easily resolve concerns arising due to accumulation of bad debts. The MKR token serves many key functionalities on the protocol, especially governance.

MKR tokens offer governance rights that can help users in regulating the development of the platform. In addition, MKR token holders are generally the last resort for borrowers. For example, if collateral does not cover the amount of DAI loans in circulation, the protocol mints MKR tokens and sells them.

- ETH, and other ERC-20 tokens like YFI, UNI, LINK and more, are used as collateral for loans, as well as paying for liquidations and network fees.

In addition to DAI, MakerDAO also supports another powerful token called MKR within its ecosystem. The MKR token manages and controls the core infrastructure of the lending platform. The investors owning MKR tokens control various elements of the protocol such as: the amount of collateral backing each CDP or the stability fee, annual lending fee or the collateralization ratio, and shut stopping the protocol in case of a crash of Ethereum price.

The token holders play a significant role in the governance mechanism of MakerDAO as well. They regulate the protocol by deciding upon the inclusion of additional collateral options along with their risk factors. They also work as the buyers of last resort for DAI lenders. This indicates the fact that if the collateral ETH stored in Maker vaults is less than the required amount, MKR is created and traded in an auction to raise the additional capital required.

The token helps to incentivize MKR holders for their sincere and responsible efforts in expanding the network. With MKR, MakerDAO emerges as a fully decentralized autonomous organization. Whenever fee charge is paid in the MakerDAO cluster, a dollar worth of MKR is purchased off the market to pay for stability fees. This hints that MKR is a deflationary asset.

> \n

Everything about MakerDAO Vaults

As you have noticed throughout the article, Maker Vaults (previously known as CDP) play a fundamental role in the operation of MakerDAO. They are the warehouses that keep cryptocurrencies that act as collateral for DAIs.

With them it is possible to interact in two ways:

- Send cryptocurrencies as collateral and obtain DAI.

- Send DAI and obtain collateral cryptocurrency.

In any case, the interaction with the vault is done in a decentralized way and without intermediaries, it is the user who interacts directly. Maker Vaults also have a schedule and rules of operation. For example, if we have sent tokens as collateral to a Maker Vault to generate DAI, this collateral will be available there, unless the price of the token we have used fluctuates beyond a point known as the “Settlement Ratio”. In case this happens, the system will liquidate the position.

Liquidating the position means that the Maker Vault will sell your cryptocurrencies trying to maintain the positive and stable relationship of the DAI as much as possible. In essence, what you seek is to avoid losses to the protocol and those who support it. This settlement is done by an automatic auction carried out by the Maker protocol under conditions that are clearly described in the interaction of users with the Maker Vaults.

Maker Clearance and Reservation Auctions

Settlement auctions and Maker reserves are two loss and damage control mechanisms for the protocol. The first one allows the system to liquidate the positions of those Maker Vaults where the liquidation relationship is negative, thus avoiding large losses in the system and maintaining DAI stability.

The objective of this is to fully cover the Vault obligations and the liquidation penalty, selling as little collateral as possible and returning the rest to the original owner of the Vault. However, under conditions of large price declines in collateralized tokens, the auction may be insufficient to cover the position. At that point, the Maker Reserve takes action placing the remainder of the position. And if this is not enough, then a debt auction is generated, in which the system increases the amount of MKR tokens to put them up for sale, and from there extract the money necessary to pay off the debts.

This elaborate mechanism is what allows DAI to maintain stability in the face of radical price changes in its collaterals or guarantees.

MakerDAO’s Risk and Collateral System

The MKR token holders provide risk parameters to every collateral asset supported by MakerDAO. This includes factors like the amount of debt to be created by the particular collateral type, the volatility the asset is likely to witness in the market, and the scenario if the collateral must be liquidated in case it fails to cover the borrowed amount.

In case of adverse market conditions where the collateral does not cover the outstanding debt, the collateral is liquidated using an automated mechanism. Automated market players called keepers who use arbitrage opportunities for gains, bid in DAI for the collateral from the vault. The amount is used to reimburse the debt and the liquidity penalty charge. The excess amount earned from the auction, after paying the debt and the penalty fee, is returned to the owner of the vault.

If the auction fails to fetch sufficient amount, the debt is termed as protocol debt and is covered by the Maker Buffer. The buffer represents the fees paid on withdrawals and the amount collected from the auction. If the Maker Buffer does not have sufficient DAI funds, debt auction is initiated and the protocol mints MKR tokens. The tokens generated are sold to the bidders for DAI to maintain the stability of the system.

Post withdrawal, the DAI stablecoins are minted and included in the total circulating supply value. When the borrowed amount taken from the vault is returned, the DAI amount associated with the vault is destroyed and detached from the supply. Due to this creation and destruction of DAI tokens, the supply value of the currency is elastic. The elasticity helps to maintain the currency’s peg to the USD. Maker Vaults require customers to overcollaterlize the vault position by a minimum of 150% to ensure safety from liquidation risks. When the collateral value falls below the borrowed value, lenders liquidate the deposited collateral to fetch their amount. As Maker depends upon volatile crypto assets for collateral, the portal needs sufficient backing to keep the solvency of DAI intact for users.

To use MakerDAO, users can move to the Maker Oasis app. The application is designed to create a Maker Vault and DAI tokens. Those willing to use the app need to have a MetaMask wallet for sure. Inside the app, one can find a list of various tokens supported by Maker as collateral. There are also metrics defining the minimum collateral ratio requirements on the portal.

After having a MakerDAO vault, users can employ their DAI tokens in multiple use cases similar to fiat. The coin is one of the most widely supported projects across crypto exchanges. This makes it an easy accessible option for trading purposes.

External Agents Working in MakerDAO

The smart contract infrastructure in the Maker protocol and Maker vaults definitely shows how MakerDAO works as a decentralized crypto lending platform. On the other hand, there is more to the working of Maker protocol than just the smart contracts. The Maker protocol depends on some external actors for maintaining their operations. Here is an outline of the external actors supporting the MakerDAO ecosystem and the value they bring to the platform.

- Keepers

Keeper in the Maker protocol is actually an independent agent receiving incentives through arbitrage opportunities for offering liquidity.

- Price Oracles

The MakerDAO crypto protocol leverages a decentralized oracle infrastructure to obtain real-time information regarding the market prices of collateral assets in the Maker Vaults. Price Oracles play a crucial role in determining the opportune moments for triggering liquidation.

- Emergency Oracles

The Emergency Oracles in Maker protocol serve as the last resort for defense against attacks on governance of the platform or other oracles.

- DAO Teams

Maker protocol also contracts DAO teams, including individuals and service providers, for ensuring governance functionalities. Interestingly, members in DAO teams are independent market players, thereby introducing credibility in governance of the protocol.

Use Cases of MakerDAO

The final highlight in any discussion on MakerDAO and its functionalities would obviously bring its use cases to the equation. One of the clearly evident use cases of Maker protocol is evident in crypto lending functionalities. The Maker protocol and its stablecoin DAI offer a productive base layer infrastructure for driving the development of other DeFi protocols.

Global organizations such as UNICEF use DAI stablecoin to obtain funding for blockchain-based open-source initiatives in social projects. Other notable practical DeFi applications powered by the Maker ecosystem refer to Uniswap and Outlet.

Furthermore, the applications of MakerDAO explained in the gaming industry can help in creation of tokenized in-game assets. The platform also focuses on introducing DAI in the art world by providing incentives to artists for trading their artwork as NFTs.

Is MakerDAO Profitable?

MakerDAo is a potential investment because:

- It is a decentralized protocol that seamlessly supports lending and borrowing in crypto.

- The holders of the MKR token become an essential part of the community as they quickly gain governance rights. On investing in MKR, users get autonomy to participate in the future decision-making processes of the firm.

- Each time a loan is repaid, equivalent worth of MKR tokens are destroyed by the network. This ensures to increase the scarcity of the token, thus. Keeping its price on a rise.

- MKR token is a profitable option for borrowers too. They can lend themselves a loan by locking their ETH assets as collateral and earning a Collateralized Debt Position.

- The protocol has its won set of risks as well. One such risk is the unceratin price crash of Ethereum that will render the collateral within the MakerDAO useless.

- There is also a risk that the volume of bad debts and non-repyaments can rise to a level where the price of MKR tokens falls.

\n

Conclusion

The basic premise of the foundations of MakerDAO crypto lending platform serves favorable prospects for its long-term growth. The Maker protocol resolves one of the long-standing issues for borrowing and lending on blockchain networks by introducing liquidity. At the same time, the assurance of trust through smart contracts also serves as a vital advantage for the Maker protocol.

With the help of two distinct tokens, i.e., DAI and MKR, the Maker protocol provides control in the hands of users. Furthermore, the emphasis on DAO and external agents is also a formidable aspect for strengthening the prospects of Maker protocol. Start learning more about the protocol and how it works practically right now.

Join our annual/monthly membership program and get unlimited access to 20+ professional courses and 50+ on-demand webinars.

*Disclaimer: The article should not be taken as, and is not intended to provide any investment advice. Claims made in this article do not constitute investment advice and should not be taken as such. 101 Blockchains shall not be responsible for any loss sustained by any person who relies on this article. Do your own research!

MakerDAO Use Cases

The Maker Protocol — aka the Multi-Collateral Dai system, or MCD — was created to unlock the possibilities of DeFi and to provide its users and developers with innovative financial tools. Therefore, the Maker Protocol, together with its Dai stablecoin, forms a vital base layer infrastructure for numerous other protocols in decentralized finance.

For example, Dai is used and accepted by numerous community-developed applications in the DeFi space. A good example is the Heritage platform from Airbus A^3. It is a blockchain-based donation and fundraising platform that allows charities to use smart contracts and cryptocurrencies to open up fundraising opportunities to a new class of potential donors.

UNICEF also uses Dai Stablecoin to enable donors to fund blockchain-based open-source explorations for social projects. Any Dai donations made to UNICEF go toward research funds and bounties for different tech projects aimed at helping vulnerable populations.

Other DeFi applications operating in the Maker ecosystem and using Dai include Outlet and Uniswap. The outlet is a high-yield alternative to a savings account, while Uniswap is a protocol designed to enable fast, efficient cryptocurrency trades of Ethereum.

Beyond applications in commercial finance, MakerDAO hopes to have an impact on regions currently suffering from hyperinflation by offering a stable alternative to volatile fiat currencies.

In the gaming industry, Dai is used for games such as Battle Racers, Axie Infinity and SkyWeaver to allow users to create tokenized in-game assets and earn rewards for the tokens on the blockchain. MakerDAO has even launched the Dai Gaming Initiative to encourage the creation of gaming apps that integrate Dai rewards.

MakerDAO is also looking to integrate Dai into the art world with the goal of incentivizing artists to trade their artworks, digitize their work as unique non-fungible tokens (NFT), and prove ownership.

MakerDAO vs. MKR

In addition to Dai, MakerDAO has another token known as MKR. The MKR token controls the MakerDAO ecosystem. Holders of the token can control different aspects of the Maker Protocol, including the amount of collateral for CDPs, annual borrowing, and shutting down in case Ethereum crashes.

MKR holders play a vital role in the governance of the Maker ecosystem. They are responsible for regulating the platform by controlling the addition of new collateral types and their risk parameters. MKR holders are also responsible for acting as the buyers of last resort for Dai loans. This means that if the collateral ETH held in Maker Vaults is less than what is required to cover the amount of Dai in circulation, MKR is created and sold in a debt auction to raise the needed amount of collateral.

MKR’s functionality is designed to incentivize responsible behavior from MKR holders. It is also responsible for building MakerDAO into a truly decentralized system.

Whenever fees are paid in the MakerDAO system, a dollar value of MKR is bought out of the market to pay for stability fees.

Is MakerDAO a CDP?

As noted above, CDP is short for Collateralized Debt Position. In simple terms, it is when a user sets aside assets to use as collateral so that the user can then take out a loan or debt against said collateral.

On the Ethereum blockchain, CDP refers to a position or loan taken through the MakerDAO smart contract.

When you open a MakerDAO CDP, you lock in Ether as collateral. You are then able to mint up to two-thirds of the US dollar value of the Ether you’ve locked up. In other words, you must have at least 150% more collateral in your CDP than the debt you wish to take.

CDP holders must pay an annual interest rate for the opportunity to create a new Dai. This fee is known as the stability fee, and it helps deter users from overinflating the total supply of Dai. Once the loan is repaid, the stability fee owed in MKR and Dai is burned.

Is MakerDAO a Good Investment?

MakerDAO is a good investment because it is a decentralized protocol. Anyone who owns an MKR token automatically becomes part of the community and gains governance rights. This means that if you invest in MKR, you will have the autonomy to decide the future of MakerDAO.

As we have mentioned previously, MKR tokens are destroyed every time a loan is paid back. This means that the scarcity of the token increases, and the price of MKR remains high. For example, between December 2020 and January 2021, the price of MKR rose from $566 to $1,200. This rapid appreciation is practically impossible in traditional financial systems.

MKR is therefore more lucrative to borrowers as well. This is because as a user, you can lend yourself a loan by locking up your ETH as collateral and creating a Collateralized Debt Position.

That being said, holding MKR also comes with its own set of risks — although most of them are hypothetical and have not occurred. The largest risk is that the price of Ethereum can crash, rendering all the collateral in the Maker ecosystem worthless.

There is also the risk that the number of bad loans and non-repayments can increase to the point where the price of MKR tokens decreases.