BanklessDAO: Membership, Liquidity and BED Index

This analysis aims to do a deep dive on 3 main aspects of BanklessDAO: 1. Membership - Growth of BanklessDAO Community 2. Liquidity Activity - Swap activity on Liquidity Pools and Platforms 3. BED Index - Going Bankless through BED Index

Background:

BanklessDAO is a decentralized autonomous organization that helps to bring forth the Bankless movement where users adopt decentralized, permissionless, and censorship-resistant technology. Through these means, user will be able to achieve finanical self-sovereignty, security and prosperity.

$BANK is the DAO's governance token which is used to coordinate activities and is distributed to reward community members for active participation in the Bankless movement.

Method

Types of users in the BanklessDAO community:

- Plebs (<35,000 BANK)

- Level 1: Member (>35,000 BANK)

- Level 2: Contributor (>35,000 BANK + invitation by Genesis Team

- Level 3: Whale (>150,000 BANK)

For this analysis, we will be focusing on the amount of $BANK tokens in each wallet address. As such, we will group Level 1 & 2 users together in the same category for this analysis in the following areas:

- $BANK Member Role changes over time

- $BANK Holder Distribution

- The no. of users with Member and Whale roles have been fairly constant the past 6 months.

- The no. of users with less than 35,000 tokens have increased by 58%.

The top 3 holders of $BANK are

Community Treasury (3Y Linear Vesting): 0xdc351121342d0d25c80203201386323c1dcc7365

Bankless LLC (3Y Vested w 6m cliff):0x844e211e291077b11221c0f18615a64f2ff19c26

BanklessDAO Treasury: 0xf26d1Bb347a59F6C283C53156519cC1B1ABacA51

Other than the BanklessDAO Treasury, the remaining top 2 holders are all vested over 3 years. This helps to ensure value accrual in the long run and prevent any significant dumping or inflation in the short term.

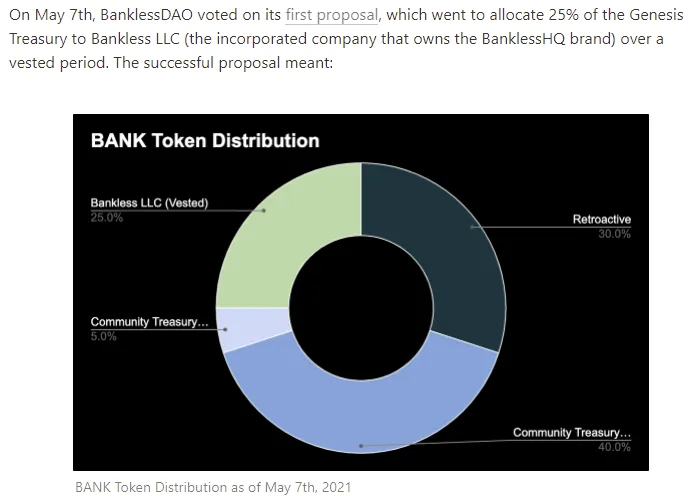

As compared to the initial token distribution shared on May 7th, 2021, the BanklessDAO Treasury has grown significantly from 5% to 18.2%. The Retroactive allocation(30%) has been nicely transferred into the hands of the community (31%) since then. In addition, there's an even distribution of tokens among the community with the top 10 holder only representing up to 10% of the total 31% held by the community.

The above pie chart shows that 93% of the BANK-WETH liquidity pool is on Sushiswap as denoted by the BANK-WETH SLP token whereas the remaining 7% is on Uniswap v2 BANK-WETH LP.

As the LP token price wasn't available and there's minimal differences between the token price of the Uniswap LP ($24.50) and Sushiswap LP ($20), the pie chart is still relatively accurate in representing the overall liquidity ratios: Uniswap-v2(60k) and Sushiswap ($800,000)

Over the past 3 months, the Sushiswap liquidity pool size almost doubled over the past 3 months while the liquidity pool size on Uniswap-v2 seems to have fallen by 62% over the past 3 months.

Note that there's 2 pools that are not included in the above analysis as they weren't available in the dex_liquidity_pool table:

- Balancer Vault (80% BANK - 20% WETH)

Contract Address: 0xBA12222222228d8Ba445958a75a0704d566BF2C8

- Uniswap V3 (BANK-WETH)

Contract Address: 0x1a80afe14143637C0b7609e6e276464e4F748014

Tokens used to swap for $Bankless token

The following analysis breaks down the tokens and platform used to swap for $BANK token. Note that only swaps with the same transaction ids are considered in the analysis, this means that the swaps were either done directly using WETH or through the swap router.

Sushiswap has the largest traded volume since the beginning out of the top 4 dexs on Ethereum followed by Uniswap v2, Uniswap v3 and finally Curve.

Across all 4 platforms, WETH has been consistently the most used token to swap for BANK. This is also to be expected since these LPs are on Ethereum with ETH as the native token and the LP pairs on all 4 platforms are BANK-ETH LP Pairs. The next few common pairs are USDC, USDT and WBTC respectively.

The above chart shows the breakdown of swap volumes into the individual LP pairs and platforms. Though it seems like some of the values for the Sushiswap LP BANK-WETH SLP and Uniswap-v2 BANK-WETH LP are too high to be true, this might be due to some anomalies in blockchain processing data. The highest volume on Sushiswap would be around $1.6M.

Nevertheless, the overall proportion with respect to each platform and pairs is likely to still be the same given that the liquidity pools are of a similar ratio.

- On overall, the amount of $BANKless tokens traded has been on the decline. There's a peak in swap volume during mid Dec'2021 which seems to be similar to the token price's recent ATH.

- Overlaying the swap volume in token quantity and USD with the average daily token price helps to identify any surges in trade volume that are solely due to price fluctuations. However, the overall trend in swap volume and token price is similar.

References for Comparison

Uniswap v3 - https://info.uniswap.org/#/pools/0x1a80afe14143637c0b7609e6e276464e4f748014 Uniswap v2 - https://v2.info.uniswap.org/token/0x2d94aa3e47d9d5024503ca8491fce9a2fb4da198 Sushiswap - https://app.sushi.com/analytics/pairs/0x2c51eaa1bcc7b013c3f1d5985cdcb3c56dc3fbc1

Background: What is BED Index Strategy

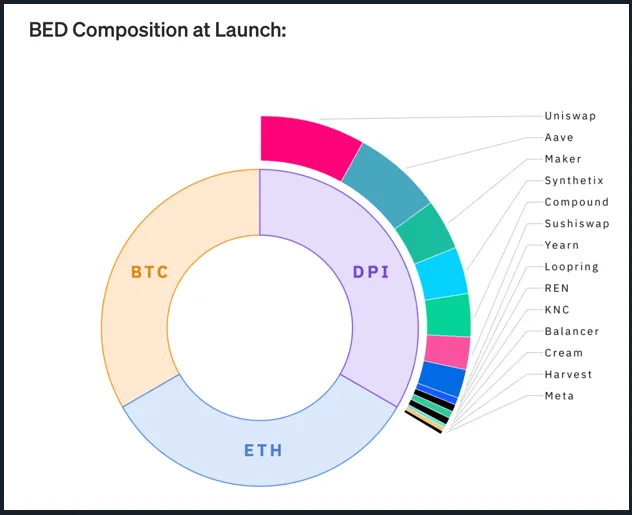

The BED Index is designed to provide a easy, hands off way to invest in a basket of diversified crypto investments: Bitcoin, Ethereum, and DeFi in equal weightage.

These 3 crypto tokens, or themes, have been carefully selected based on their theses:

- Bitcoin - "Digital Gold" / Store of Value

- Ethereum - Programmable Money

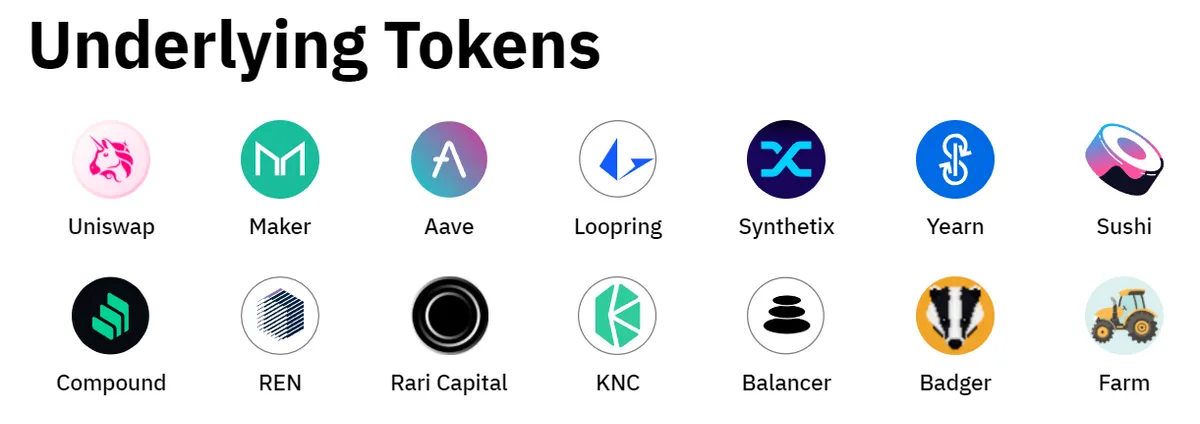

- DeFi - DeFi Pulse Index (DPI) consisting of reputable DeFi projects like Uniswap, Maker, Aave, etc

Token Price Action

Note that in this analysis, we will be using mSPY to represent S&P 500 and mQQQ to represent Invesco QQQ ETFs. These are mirrored Assets issued by the Mirror Protocol on the Terra Blockchain. Even though there's some price difference between the market price of SPY and mSPY, and like wise for QQQ and mQQQ, the overall price action are similar.

- The BED Index's ATH in Sep-Nov was likely due to ETH's and BTC's ATH, since then, it has been on the decline. Given that crypto has been pumping for the past couple of months before that, this would not be surprising. In addition, this could be due to several macro-economic conditions or just users taking profit at the ATHs. Macroeconomic conditions that could have contributed includes concern over FED hiking interest rates, increasing crypto regulations, and many more.

- For the traditional markets, both SPY and QQQ peaked in early Jan before declining over the past 2 months. This could also be due to investors taking profits, especially after a 16% growth in 2020 followed by a 27% growth in 2021, and investors selling stocks during Jan to push their tax liability into the following year.

The above chart shows a better visualization of the relation between the SPY and BED Index, the QQQ and BED Index. The overall trend of QQQ and SPY are mostly the same and hence the ratios perform similarly.

From the chart, it can be seen that since the bottoming out of the SPY/BED ratio in May (previous BTC/ETH ATH), the ratio has been rising since then. This would likely continue till the various FED meetings and announcements in Mar and Apr.

Many of the underlying tokens in the DPI index have been on the ETH chain for quite some time (min 180 days to be exact), however, this also means that many of these protocols have been around for quite sometime and excludes several of the new DeFi 2.0 innovations, crypto options like dYdX and new L0 chains like Cosmos, blockchain bridges and many more.

However, it is also due to this stringent criteria, tokens that are added to the index are all of a certain caliber and do not belong projects that exhibit ponzi-like tokenomics.

For those more seasoned crypto traders/users, I'm sure you have much better ideas on how to diversify your portfolio according to this year's thesis than to rely on the BED Index.

Conclusion

Based on the analysis above, it does seems like the market has been bearish and BED Index may not be the best way to have invested in the short term given the overall decline with respect to traditional indexes like SPY and QQQ.

However, I'm still confident that BED Index is still a good and easy way for beginners to diversify their current portfolio to obtain some exposure to the crypto markets. This would save the user from alot of headaches from meme coins, rug pulls and trying to navigate the various blockchain and dapps. Cryptocurrency is here to stay and many of its benefits were for all to see especially in the recent crisis in Ukraine. Decentralised, permissionless and censorship-resistant technology is all part of the new technology age known as web3.

As the famous saying goes: We are still early. WAGMI. LFG.

References

BanklessDAO

https://www.bankless.community/ https://bankless.notion.site/bankless/BanklessDAO-82ba81e7da1c42adb7c4ab67a4f22e8f https://snapshot.org/#/banklessvault.eth/proposal/QmdoixPMMT76vSt6ewkE87JZJywS1piYsGC3nJJpcrPXKS

Comparison for Liquidity Analysis

Uniswap v3 - https://info.uniswap.org/#/pools/0x1a80afe14143637c0b7609e6e276464e4f748014 Uniswap v2 - https://v2.info.uniswap.org/token/0x2d94aa3e47d9d5024503ca8491fce9a2fb4da198 Sushiswap - https://app.sushi.com/analytics/pairs/0x2c51eaa1bcc7b013c3f1d5985cdcb3c56dc3fbc1