Sushi Slippage

In DeFi, the lack of a centralized market maker and deep liquidity coupled with the slow transaction response, act strongly against faciliating orderbook trading. In 2017, Bancor came up with the Constant Product AMM, now used by two of the greatest DEXes on Ethereum, Uniswap and Sushiswap.

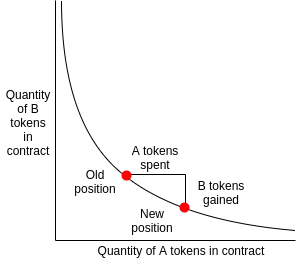

The concept behind the system is pretty simple. There exists a constant K. The product of number tokens in the pool, should always be equal to this constant K. Say x and y are the number of tokens, The exchange price P of the token is the ratio between the two token volumes. Then

> xy = K

Let us take an DAI - USDC example. Say there is a pool with 100 DAI + 100 USDC .The value K is

> K = 100 x 100 = 10000

and

> P = 100 / 100 = 1

When a user wants to swap 10 DAI for USDC , he adds 10 DAI first to the pool. Then the protocol calculates the amount of USDC to be released to keep the K constant.

>K = 110 x [USDC] = 10000

and

[USDC] = 10000/110 = 90.90

The excess 9.1 USDC is given to the user.

The de-merits of this model is clear. The user expects 10 USDC in return, but only gets 9.1 USDC. This 0.9 USDC is the slippage of the swap.This slippage is dependent on the Liquidity in the Pool, and the number of tokens swapped in. Higher the Liquidity, lower the slippage. Higher the number of tokens swapped in, higher the slippage.

In this dashboard, we will look at the necessary evil the median slippage between Sushiswap and Uniswapv3.

We calculate the slippage from each swap by comparing their USD valuation. Simply subtracting the USD value out from the USD value in and finding its percentage should do the trick. >( USD_in - USD_out ) x 100 / USD_in

Inorder to make it a fair comparison, only the top 5 pools from both the Protocols will be used for this analysis.

Let us look at the median slippage now.

From the plot above, we can see that Sushiswap has consistently had higher slippage than that of Uniswapv3. Why could this be so ??

There are three reasons that it could be so ...

- Concentrated Liquidity : Concentrated Liquidity on Uniswap allows increased liquidity within certain ranges, which means it simulates deep liquidity across the Pool. This feature of Uniswap increases its slippage efficiency

- Swap volume - Uniswap has more activity in terms of swaps made. This means, the price is much more actively rebalanced than Sushiswap. This constant fluid rebalancing means, Uniswap Liquidity is usually replenished after big swaps, which reduces slippage, as liquidity lost in swapping is replenished immediately.

- Pool Value Locked - The large pool sizes of Uniswap compound its concentrated liquidity. As slippage is a function of Pool liquidity, Uniswap is bound to have the better slippage.

We can see from above that the new-tech as well as first mover advantage have strengthened the hand of Uniswap extremely well. One must also note that, two of the Pools from Uniswap used in the analysis or stable pair, which usually have much better arbitrage conditions that other pairs. Yet, Sushiswap despite being at a disadvantage hasn't been far off.