Redemption Arc

Q177. Explore the limitations of redemption on Terra, i.e. the burn and mint mechanism. In what scenarios would the ability to burn & mint be insufficient for demand? Using data, illustrate occasions where these scenarios have occurred or come close to occuring. There are a number of ways to do this; one approach is to quantify a “Redemption Utilization”, i.e. a performance metric that encapsulates the extent to which demand for redemptions outstrips or comes close to the programmed caps, and then to explore the number of days over a specified time period that this metric has crossed a concerning threshold.

The TLDR

> In order to protect against oracle manipulation attacks it’s important that the on chain market not be more liquid than markets off chain.

- From "Terra on-chain liquidity parameters", an analysis of Jump Trading

After the disasterous crypto crash of May 2021, UST lost its peg with the dollar. At one point, the price was as low as USD 0.85. As a result the "Luna Community" (in quotes because a small number of validators control a big block of votes), took some actions to adjust the stability of the Terra ecosystem.

The screenshot of coingecko.com's chart shows that in general, even before the mid-May crash, that UST has much improved its range, and normally tends to drift above the price and not below which seems bullish to me but I am not sure! This is hardly proof of an infallable system, where UST is now completely immune from losing its peg, but it certainly is encouraging, to the "lunatics".

In reality, the system behaved as designed. Because UST is not collateralized in the traditional sense of the word anyway, the tradeoff is that it will occasionally drift apart faster than a collateralized stablecoin. That said, the long term adoption of UST is in jeopardy, if the behavior observed during that infamous week in May were a common occurence.

Things to understand:

- Luna is not collateral. It derives its value from the Terra ecosystem. Its role is to absorb the volatility of the market.

- The protocol restricts minting operations so as to protect against a "front running attack". However, as was demonstrated, this throttled arbitragers ability to take action quick enough to maintain the peg.

- Once the price of UST drifts far enough away from its peg, exchanges outside of the Luna ecosystem can now profitably afford to arbitrage themselves, causing further decline and a spiral effect ensues.

- "The UST algorithmic peg is a function of the parity between the off-chain liquidity of LUNA/UST and the on-chain liquidity parameters for the redemption of UST/LUNA." TerraUST twitter account tweet – May 25, 2021

The key here is to make the liquidity of the on-chain supply less than but close to the off-chain liquidity. There is a 'goldilocks' value. There is a need to limit the minting and burning capacity of Luna, as well as the

The problem with liquidity off chain outpacing that of on-chain is that whales can deliberately up the price of an asset with an off-chain purchase and then, when the price moves, they then dump their assets on-chain. This strategy doesn't work when the off-chain market is liquid enough, because it costs too much in slippage to move the price.

The best way to wrap your head around "liquidity" is to think about the bid vs ask spread. We want that to be small. The big trading cost, especially if you are a whale, is the slippage between the bid and the ask. You want the difference to be small. In tradfi, this difference should not be more than 5% of the price of the asset and certainly no more than 10%.

This article assumes a basic understanding of the burning/ minting process on Terra, where Luna, the fuel (think Ether for gas, only a different chain) of the Terra) is "burned" (dissapeared) to "mint" UST and vice versa. For a more detailed explanation (and to flaunt my grand prize winning submission) you can read this grand prize winning submission by your's truly.

You are also expected to know what a "whale" is and what "FUD" is. You should do your best to pretend like you understand concepts like "volume", "volatility" and "liquidity".

Full disclosure: I have a massive 300 dollar portfolio living on the Terra ecosystem. This is mainly because that's where Flipside sends me my bounty rewards when I investigate the Terra Ecosystem and does not necessarily imply an indorsement (or non indorsement) of the Terra protocol and its uses.

This is not financial advice. No animals were harmed during the production of this article.

Chart courtesy coingecko.com

Traders are sometimes irrational and crypto traders are often irrational. Youth and the inherrent volatility of assets representing disruptive technology will do that to you. When UST went down in value, the savvy players seized the opportunity to exploit the price differential. In fact, because of the wider-than-usual gap between UST and USD, the long term way of exploiting this opportunity, as opposed to minting and burning as is necessary, is to simply buy low (swap Luna for UST) and wait for the UST price to recover and then sell. Now all of a sudden a week's time doesn't seem so bad. Fudders gonna fud.

As mentioned, the "community" rapidly analyzed and reacted to the spike. An official TerraUST, referenced above, called for action, explained the phenomenon and, accompanied by "Proposition 90", introduced by Jump Trading proposed to main adjustments.

- An increase in the minting limit making UST less subject to the shenanigans described above.

- A decrease in the voting period, so that the price will adjust faster during times of extreme volatility.

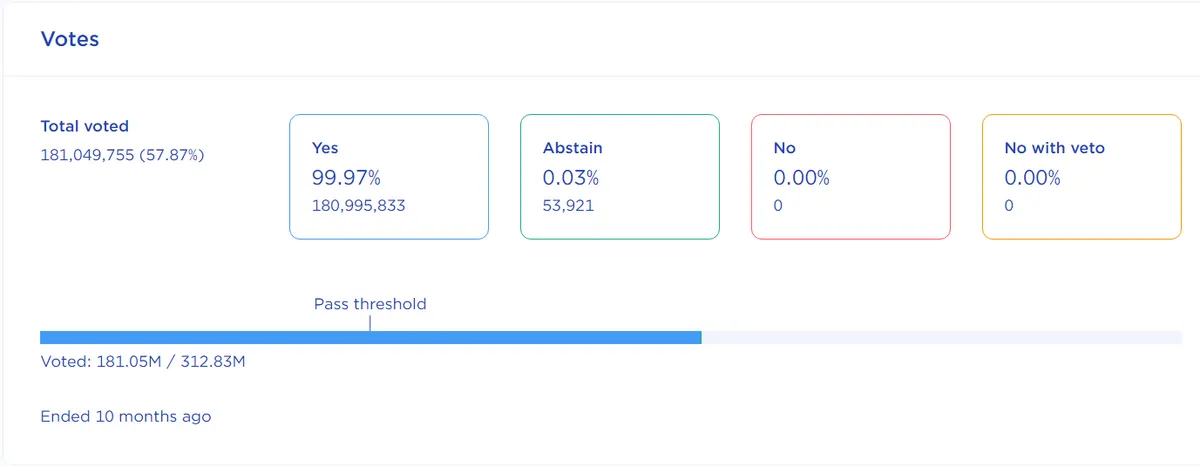

Such adjustments will probably also be necessary in the future. Presumably these will not be contreversial. This probably has something to do with the aforementioned, somewhat rigged voting process, but on the other hand, the system is set up in such a way where the validators have a stake in seeing stability. The validators also comprise most of the whale community. Here are the not very suspenseful results of Proposition 90:

Jump Landing published an analysis (cited earlier) where they first examined the order book data from "off chain" (I expect this was mainly CEX data) then they ran simulations "on chain", trying various pool sizes and then charting pool size vs bid size. The goldilocks curve was at 5%. They also determined that 20 seconds was a better pool decay_time, based on a rough estimate of the average daily volume which they claimed ( with no real methodology explained ) is proportional to the liquidity. The proposition was proposed in January, but the proposition passed after the may 19 black swan event. The claim was that had these measures already been in place, the peg would not have been broken. We are left at their word for this as well.

In any event, with the prodding of Do Kwon, and the faith in the analysis of Jump Trade, the measure passed and as indicated by the UST price chart, so far seems to have had a positive effect.

In this article, I attempted to shed some light on the factors and metrics involved and the parameter tweakings at the disposal of the Terra protocol to consider the factors involved in maintaining the UST peg to the dollar.

The key time period we concerned ourselves with was the one week period after the May 19 BTC capitulation event. We examined some key metrics including

-

The price of UST as compared to USD – the main goal being to keep this ~0. This is the main metric.

-

the price volatility of Luna. – things get sticky when there is a rapid decline. No crypto is immune to greater market forces no matter how strong their fundamentals.

-

the on-chain transaction volume

-

the order flow of central exchanges.

We learned that in order to keep the most important metric (UST price close to 0), the key consideration is that the on chain liquidity must not exceed the off chain liquidity. By increasing the cap on minting and burnings — but not by too much.

Following the week long divergence from the peg, the tweet from TerraUST and accompanying study by Jump Trading, a proposal addressing this issue, proposition 90 passed unanimously with a handful of abstentions. Since that time, the price of UST has stayed within a noticably closer range.

Thanks for reading!